Life Insurance with No Waiting Period

last updated on January 31, 2026

last updated on January 31, 2026Life insurance with no waiting period means your policy pays the full death benefit from day 1 instead of refunding premiums during the first 2 years.

Affordable coverage is available without requiring a waiting period for benefits to take effect.

You pay the first premium installment, and you are entitled to get the full benefits of the policy even if you die within a few days.

In this article, I’ll help you find the best burial coverage for your needs and assist you in qualifying for a life insurance policy without a waiting period today.

WHAT “NO WAITING PERIOD” REALLY MEANS

No waiting period means the insurer pays the entire benefit immediately after the policy starts, not just a refund if death happens early.

That’s not always true.

A waiting period is a delay built into some policies where the insurance company won’t pay the full death benefit right away if you pass away within the first two years. Instead, your family only gets back the premiums you paid, plus a small amount of interest.

True first-day coverage differs from what I assist people with at The Final Expense Guy.

1st-day coverage means your life insurance policy will pay the full death benefit from the very first day it takes effect. If your policy started on a Tuesday and you passed away on the following Wednesday, your family receives the entire benefit amount.

It’s the best life insurance available with the lowest rates.

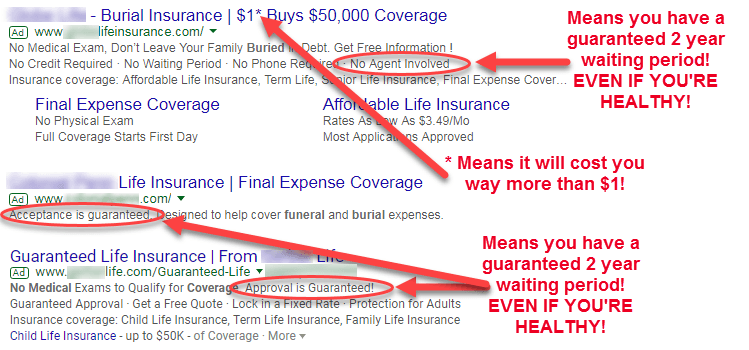

Many insurance companies or agents advertise their plans as “coverage begins immediately,” but that phrase can also be used deceptively.

With many companies, they may start collecting your payments immediately, but that doesn’t mean your full benefit is active from day one. The fine print often says that if your death is due to natural causes (medical event, disease, etc.), it is not covered until after a MANDATORY two-year period.

Every year, I see families left shocked because they believed they had full coverage when, in fact, they didn’t. The reality is that about 97% of people I help qualify for first-day coverage.

WHAT LIFE INSURANCE WITH NO WAITING PERIOD COSTS

First-day coverage costs depend on age, health, and tobacco use, with level premiums that stay the same for life.

Since these policies pay 100% from day one, the insurance company will check that you’re reasonably healthy before offering you any approvals.

At the Final Expense Guy, even with significant health conditions, most people I help qualify for affordable 1st-day coverage rates.

Here’s a realistic look at average monthly rates for $10,000 in first-day coverage for non-smokers:

Rates stay level for life and never change.

Unlike term life, which eventually expires, your premiums and benefits remain unchanged as long as you keep your whole life policy active.

POLICIES THAT CLAIM “NO WAITING PERIOD” BUT DELAY PAYOUTS

Many policies marketed as immediate coverage actually delay full benefits for 1–2 years through graded or guaranteed-issue rules.

Some companies use soft phrases like “benefits begin immediately” or “coverage starts the day you’re approved.” That wording sounds like first-day coverage, but it often only means they’ll refund your premiums for two years before paying full benefits.

Here are the biggest red flags to watch for:

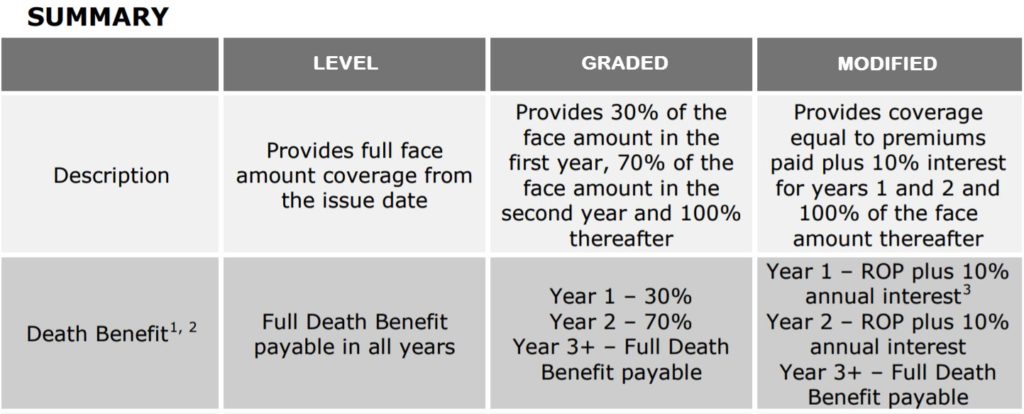

- “Graded Benefit” or “Modified Benefit.”

These plans pay 30-40% of the death benefit in year one, 70-80% in year two, and 100% after that. - “Return of Premium plus Interest.”

This means you’re not insured yet. You’re only getting your money back with a small amount of interest if you die early. - “Guaranteed Acceptance, No Health Questions.”

Every guaranteed-issue plan includes a two-year waiting period for natural death. - “Immediate Coverage” Ads on TV.

Almost every one of these commercials is for a lead vendor or term life insurance that goes up in price every 5 years.

To help you see the truth at a glance:

If a company or agent won’t ask health questions or can’t explain the waiting period clearly, walk away.

Real first-day coverage is available for almost everyone with a decent health history.

💡 The $9.95 Mailer That Wasn’t Insurance

Colonial Penn guaranteed-acceptance coverage implied immediate protection, resulted in a 2-year delay for natural death, and led Linda to believe her family was fully covered.

Linda, age 72, called me after finding a bright postcard in her mailbox that promised acceptance with no health questions and simple enrollment over the phone. The agent told her coverage started right away, and she assumed that meant the full benefit would pay if anything happened.

The policy language told a different story. The first 24 months only refunded premiums plus interest for natural causes, which meant her family wouldn’t receive the full benefit if she died early from illness.

I reviewed her medications and recent medical history, walked through the underwriting rules, and moved her to a simplified-issue whole life policy. Her $15,000 benefit is immediate and intended to cover cremation, final medical bills, and unpaid household expenses from day 1.

ARE COMPANIES LIKE OPEN CARE OR COLONIAL PENN “NO WAITING PERIOD” PLANS?

Popular TV and mail-order brands often sell guaranteed-issue policies that delay full payouts despite sounding immediate.

The same goes for many companies that advertise through TV commercials or Facebook ads. They make their offers sound official by saying things like “new government program” or “state-regulated coverage.”

What they often do is connect you with high-priced guaranteed-issue policies that always have a two-year waiting period.

Colonial Penn is a great example. Their $9.95 plan is guaranteed acceptance, but it’s not first-day coverage. If you pass away during the first two years from natural causes, your family will receive only the premiums you paid, plus 7% interest.

That’s not true life insurance protection. That’s a refund-only policy for the first two years.

Many of these programs are marketed toward seniors who believe “guaranteed acceptance” means “immediate benefit.” It doesn’t.

The reason those plans don’t ask any health questions is that they know they’re delaying the full benefit for two years.

Here’s how they compare to legitimate first-day coverage carriers:

This is why many people think they have real first-day coverage protection when they don’t.

If your plan doesn’t ask health questions when you apply, it’s automatically a two-year wait policy. Always read the policy before you buy and look for the words immediate full benefit in writing.

💡 The $9.95 Mailer That Wasn’t Insurance

Colonial Penn guaranteed-acceptance coverage implied immediate protection, resulted in a 2-year delay for natural death, and led Linda to believe her family was fully covered.

Linda, age 72, called me after finding a bright postcard in her mailbox that promised acceptance with no health questions and simple enrollment over the phone. The agent told her coverage started right away, and she assumed that meant the full benefit would pay if anything happened.

The policy language told a different story. The first 24 months only refunded premiums plus interest for natural causes, which meant her family wouldn’t receive the full benefit if she died early from illness.

I reviewed her medications and recent medical history, walked through the underwriting rules, and moved her to a simplified-issue whole life policy. Her $15,000 benefit is immediate and intended to cover cremation, final medical bills, and unpaid household expenses from day 1.

COMPANIES THAT OFFER FIRST-DAY LIFE INSURANCE COVERAGE

Several A-rated insurers offer real first-day coverage when you qualify through simplified health questions.

Here are a few of the most reliable:

I always look for carriers with solid A.M. Best financial ratings, meaning they’re financially stable and reliable when it comes time to pay claims. These are the same companies that independent agents use to qualify seniors for real, first-day protection.

The best company for you will always depend on your health history. For example, Aetna is more lenient with lung issues, while Family Benefit is ideal for individuals with diabetes or those taking medication for heart and blood pressure conditions.

WHO QUALIFIES FOR NO-WAITING-PERIOD LIFE INSURANCE

Most adults with common, controlled health conditions can qualify for immediate coverage without a medical exam.

Simplified-issue underwriting was designed for seniors and families with the most common health conditions that often develop with age.

You can usually qualify if you:

- Are between 40 and 85 years old

- Live independently or with minimal daily assistance

- Have controlled medical conditions such as diabetes, hypertension, or high cholesterol

You might face a waiting period only if:

- Need help with Activities of Daily Living

- Use full-time oxygen for COPD

- Have active cancer treatment

- Reside in a nursing facility

- Recently diagnosed with a terminal illness

The underwriting questions are straightforward and can be completed in under five minutes with most companies.

Approvals happen the same day with the Final Expense Guy, and your full death benefit is active immediately upon your first premium payment.

HOW FIRST-DAY COVERAGE WORKS

First-day coverage uses simplified underwriting to activate full benefits as soon as the policy is issued and paid.

These life insurance policies don’t require a medical exam. Instead, the insurance company asks a short list of health questions to determine your eligibility.

If you can answer “no” to certain high-risk conditions, the company will approve you instantly.

That approval means your full coverage amount becomes active immediately upon issue, not after two years.

These health questions often focus on things like:

- Cancer in the past two years

- Recent heart attacks or strokes

- Current oxygen use

- Terminal illness diagnosis

- Kidney failure or dialysis

Even if you’ve had health issues, the majority of health conditions will still qualify for first-day coverage.

Controlled diabetes, high blood pressure, high cholesterol, and even past heart problems are often accepted (acceptance depends on each individual insurance company).

Because these policies are medically underwritten (not guaranteed issue), they carry lower risk for the insurer, and they pass that financial savings on to you.

Your life insurance rates never increase, and your coverage never expires as long as premiums are paid.

The underwriting process often takes only minutes. A licensed agent (like me) collects your information, submits the application electronically, and most approvals happen right away over the phone.

That means your family can be fully protected before you hang up the phone.

TYPES OF LIFE INSURANCE THAT OFFER NO WAITING PERIOD

Term, whole life, and final expense insurance can all provide immediate coverage when approved.

Here are the main types that can include no waiting period options:

Term Life Insurance:

Designed for people under 60 who want large coverage amounts at a low cost. It’s medically underwritten, meaning the company may ask health questions or require a brief phone interview. If approved, term life pays the full death benefit immediately from day one.

Whole Life Insurance:

Permanent coverage that lasts for life, usually with smaller benefit amounts. Many simplified issue whole life policies offer first-day coverage with no exam. These are ideal for seniors or anyone who wants lifetime protection without medical testing.

Final Expense Insurance:

This is the most common form of first-day coverage. It’s a type of whole life insurance designed to cover funeral costs, debts, or end-of-life expenses. As long as you can answer basic health questions, your full benefit can start from the very first day.

Most people over the age of 50 choose final expense whole life policies because they’re simple, affordable, and guaranteed never to expire. These plans are designed for seniors.

IS “STATE-REGULATED LIFE INSURANCE” REAL OR JUST A MARKETING TRICK?

“State-regulated” life insurance is marketing language, not a government program or special benefit.

But these mailers are not government programs. They’re marketing tools, and are often considered a SCAM by the people who receive this junk mail.

Your state’s Department of Insurance technically regulates every life insurance policy in the United States. That regulation only means companies must comply with state laws regarding licensing, pricing, and solvency. It does not mean the state created or sponsors the policy.

To be clear… no state or federal government sells private life insurance to the public.

Yet many advertising agencies exploit the phrase “state-regulated” to make their offers sound as though they are endorsed or approved. The goal is to get you to call a toll-free number, where a call center agent can sell you a waiting-period policy that benefits them more than you.

If it were truly a government program, it would originate from official agencies such as the Social Security Administration, the Department of Veterans Affairs, or your state’s insurance department website, not a third-party mailer.

These mailers are often sent out by companies or agents that only sell guaranteed acceptance and two-year waiting period plans, which are often disguised as “state benefits.” They target seniors who are more inclined to trust anything that looks official from the state or government.

You can verify whether a company is legitimate by checking its license with your state’s Department of Insurance or by confirming its A.M. Best financial rating.

If you want protection that’s real and active from day one, work with a licensed independent agent like the Final Expense Guy who can connect you directly to top-rated insurers, not a marketing group that pretends to represent your state.

🔍 The “State-Regulated” Postcard Confusion

A state-regulated mailer used compliance language, routed Margaret to a lead vendor, and led her to think the plan was endorsed and active from day 1.

Margaret, age 75, responded to a postcard that looked official and referenced her state insurance department. The phone number connected her to a sales desk that skipped health questions and framed the offer as a limited enrollment benefit.

The missing detail was that no state agency was involved and the plan was guaranteed issue with a mandatory waiting period for natural death. The wording created trust while avoiding any plain-language explanation of delayed payouts.

I verified her independence and stable health, explained what “state-regulated” really means, and placed her with a first-day coverage carrier. Her $25,000 policy is immediate and intended to cover funeral services, cemetery costs, and final household obligations from the day the policy starts.

HOW TO AVOID LIFE INSURANCE SCAMS

Real life insurance comes from licensed agents and named insurers, not lead vendors or vague ads.

Most “instant approval” or “state-regulated program” ads are generated by lead vendors, not insurers. Their only job is to collect your data and sell it to call centers.

Real first-day coverage is only available through licensed agents, such as the Final Expense Guy, who represent legitimate companies.

You can verify any agent by visiting your state’s Department of Insurance website or checking the National Association of Insurance Commissioners (NAIC) license lookup tool.

Both sources list active licenses, company appointments, and complaint records.

Another good way to spot a scam is to ask a simple question: Who underwrites this policy?

If the person cannot provide you with the insurer’s name and A.M. Best rating, that’s a warning sign.

Be cautious of these phrases:

- “State-regulated program”

- “Government-approved life insurance”

- “No health questions”

- “Guaranteed acceptance for everyone ages 40-85”

Those phrases almost always mean it’s a two-year waiting period plan with higher premiums and lower benefit amounts.

When you speak with a legitimate and quality broker, you should receive a written quote that clearly displays the company name, the policy form number, and the exact death-benefit amount from the outset.

HOW TO APPLY AND GET APPROVED SAME DAY FOR LIFE INSURANCE?

Most first-day policies can be applied for, approved, and activated in a single phone call.

The process is simple:

- A licensed agent asks a few health and lifestyle questions.

- Your answers are entered into an electronic application.

- The company runs instant checks through prescription databases and health records.

- Within minutes, you receive a decision and your policy number.

No medical exam. No doctor’s visit. No waiting for approval letters in the mail as most insurers use electronic underwriting these days.

That means the system instantly compares your health answers with their database and issues an approval or denial on the spot. If approved, your coverage starts after your first premium payment.

You’ll sign the application digitally, choose a beneficiary, and set up automatic payments. The policy arrives in the mail within two weeks, and your protection is already active.

Every insurer has slightly different rules. The wrong application could mean paying for a plan with a waiting period you didn’t want or need.

BEST ALTERNATIVES IF YOU CAN’T QUALIFY FOR FIRST-DAY COVERAGE

Guaranteed-issue policies provide coverage when health is severe, but they delay full benefits for 2 years.

The fallback choice is a guaranteed issue whole life policy. These plans are available to everyone aged 50 to 85, regardless of medical history.

The catch is the two-year waiting period for health emergencies or natural death causes.

During those first two years, your family only receives a refund of premiums plus interest if you pass away. Accidental death, however, is covered from day one.

Here’s how guaranteed issue compares to simplified issue (first-day coverage):

Guaranteed issue should be your last resort, not your first choice. It’s better than leaving your family unprotected, but you should always see if first-day coverage is possible first.

GOVERNMENT VS. PRIVATE LIFE INSURANCE

Government death benefits are limited and small compared to private life insurance payouts.

The government doesn’t sell private life insurance. Every “state-regulated” or “federal burial plan” you see advertised is sold through a licensed insurance company.

Here’s what the government actually offers:

- The Social Security Administration provides a one-time death benefit of $255.

- The Department of Veterans Affairs offers VALife, SGLI, and VGLI to active-duty members and veterans. These programs have specific eligibility requirements and limited coverage amounts, and are often so overpriced, they are one of the worst choices.

Private life insurance, on the other hand, pays directly to your beneficiaries, in the full amount you choose, and often much faster than government programs.

Here’s how they compare:

Government programs offer limited assistance, but they typically do not cover funeral costs or provide income replacement for families. Real protection that pays reliably comes from private carriers that specialize in first-day coverage.

WHY MOST AGENTS DON’T OFFER FIRST-DAY COVERAGE

Many agents push waiting-period plans because they’re easier to sell and pay better commissions.

Many agents don’t even offer first-day coverage because it doesn’t pay them as much or requires more product or life insurance underwriting knowledge.

Captive agents are those who work for a single insurance company and are restricted to selling only that company’s products. If their carrier doesn’t offer first-day coverage, they don’t have it to sell.

The result? You get a terrible policy with a waiting period that benefits the company more than your family.

Call centers or internet advertising are even worse.

Call centers or internet-based insurance companies train their agents to sell guaranteed-issue plans because they require no underwriting, allowing rookie agents to close sales quickly. It’s volume over value. The agents earn their commissions whether you get adequately protected or not.

Experienced independent brokers, such as The Final Expense Guy, work differently. We contract with multiple A-rated companies and tailor each policy to your health and budget.

If you have diabetes, we know which carriers overlook it. If you have a heart condition, we know which underwriters are lenient. This knowledge can mean the difference between a two-year wait and the best protection on your first day.

Another reason many agents don’t offer first-day coverage is turnover.

More than 90% of new agents leave the business within a year. They never stay long enough to learn the underwriting systems or the differences between modified and immediate benefit plans.

That’s why you should always work with an agent like the Final Expense Guy. Longevity in this business means stability, knowledge, and accountability.

HOW TO COMPARE LIFE INSURANCE COMPANIES PROPERLY

Smart comparisons focus on financial strength, underwriting flexibility, and complaint history, not just price.

Start with A.M. Best ratings. This independent agency grades insurers on their ability to pay claims. Anything A- or higher is considered financially strong.

Then check the National Association of Insurance Commissioners (NAIC) complaint index. It measures the number of customer complaints a company receives in relation to its size. A lower score means better service.

You can also verify licensing through your state’s Department of Insurance and confirm customer reviews on the Better Business Bureau (BBB) website.

When comparing, focus on three things:

- Financial Stability: Strong ratings mean guaranteed claims payment.

- Underwriting Flexibility: Choose carriers that accept your specific health conditions.

- Customer Service: Look for companies with low complaint ratios and fast payout times.

A policy is only as good as the company standing behind it. Cheap premiums mean nothing if your family struggles to get the death benefit.

SHOULD YOU CHOOSE LIFE INSURANCE WITH NO WAITING PERIOD?

Immediate coverage is the right choice if you want your family protected in full from the first day.

Life insurance with no waiting period is the only kind that guarantees your family receives the full payout from the very first day your policy starts. It’s straightforward, honest, and reliable.

You’re paying for quality life insurance, not a refund plan that makes your loved ones wait two years to get what you thought they were covered for.

These plans don’t rely on gimmicks or “government-approved” marketing phrases. They’re real, permanent policies that lock in your rates for life.

Your premium will never increase, your coverage will never decrease, and your family will never have to worry about whether the policy will pay out in the future.

The peace of mind is immediate. So is the protection.

If you’re unsure what you qualify for, the simplest step is to speak directly with a licensed independent broker, not a call center. You’ll get the truth about what’s available, what’s affordable, and which companies fit your health best.

Call 888-862-9456 or visit FEXGUY.com to compare real first-day coverage quotes and make sure your family is fully protected.

FREQUENTLY ASKED QUESTIONS: LIFE INSURANCE WITH NO WAITING PERIOD

Is there any life insurance that starts immediately?

Simplified-issue whole-life policies can start coverage the same day you’re approved. It’s called first-day coverage, and it’s available through simplified-issue whole-life insurance. If you can answer basic health questions (like “Do you currently live in a nursing home?” or “Are you receiving hospice care?”), you can qualify for coverage that begins the moment your policy is approved.

Does life insurance start straight away?

Some life insurance starts immediately, and some doesn’t. Guaranteed-issue policies (such as Colonial Penn) typically have a waiting period. First-day coverage policies begin immediately upon approval and payment of your first premium.

Does life insurance kick in right away?

Most seniors qualify for plans that pay full benefits from day one. These are the plans 97% of seniors qualify for – they pay full benefits from day one.

Is there any insurance with no waiting period?

First-day coverage is available when you qualify for simplified-issue whole-life insurance. The key is to avoid “guaranteed acceptance” plans and work with an independent agent who can match you with carriers offering immediate protection.

Which life insurance doesn’t have a waiting period?

Several carriers offer day-one coverage when you qualify through simplified-issue underwriting. These are the real first-day-coverage policies that pay out immediately upon approval.

What insurance does not have a waiting period?

Simplified-issue whole life is the type of policy that can start with no waiting period for qualified applicants. It’s permanent, affordable, and never expires as long as you pay your premium.

Does TruStage have a two-year waiting period?

Most TruStage policies use a graded benefit period that delays full payout for $2 years. They sell guaranteed-issue plans that refund premiums plus interest if death occurs during the first two years.

Which insurance has a zero waiting period?

A first-day-coverage whole-life plan from a top-rated carrier can pay immediately when you qualify. These companies offer immediate coverage to qualified seniors, even those with mild health issues such as high blood pressure or controlled diabetes.

8 Comments

Abzal Mohammed

Looking for Life insurance I just turn 84 years on February 22nd

(1) whole life for $10,000 or $15,000. or

(2) Term Life if available.

Janie reddell

Coverage for final expess

Final Expense Guy

Janie – Visit this page to get information and a quote – https://fexguy.com/free-quote/

Vester Robinson

Just checking around for the right quote

Scooter Sumpter

Need a quote for whole life $5000 no waiting please.

Final Expense Guy

Hi Scooter! You can get pricing and coverage amounts by calling us at (888) 862-9456 or by using our quoting software on this website page – https://fexguy.com/free-quote/

Jeffrey Hamner

wouldn't let me finish application process

Final Expense Guy

Jeffery – try this – https://fexguy.com/free-quote/