Autism Burial Insurance

Here’s the Bottom Line:

• Autism doesn’t automatically disqualify you from life insurance approval

• Mild, independent cases often qualify for standard or first-day coverage

• Severe cases may lead to higher costs or limited policy options

• Guaranteed issue plans cost more and delay full payout for 2 years

• Applying without a strategy can lead to declines or overpaying

Getting burial insurance with autism depends on how the condition affects daily life, not just the diagnosis itself. Insurance companies look at independence, stability, and overall health when reviewing an application. Many people with mild or well-managed autism can qualify for whole life or burial insurance with immediate coverage and normal rates. More complex cases may be limited to higher-cost options or guaranteed issue policies with waiting periods. The biggest mistake is assuming autism blocks coverage entirely. It doesn’t. The details of your situation determine what you qualify for.

Get a quote on this page by completing my quote request form now.

Autism Burial Insurance Key Insights

- First Day Coverage for Most: You don’t have to settle for a two-year wait; as long as you can manage your own affairs, I can usually find you immediate coverage that protects your family from day one.

- Independence Equals Better Rates: If you live on your own and don’t need help with daily activities like bathing or dressing, you can usually qualify for the lowest-priced plans available.

- Autism Isn’t a Deal-Breaker: Most insurance companies don’t even put autism on their health checklist, meaning your brain being “wired differently” won’t stop you from getting affordable coverage.

- Other Health Issues Matter More: Things like seizures or heart health impact your price much more than an autism diagnosis, so it’s important to look at your whole health history.

- Stable Meds Help Your Case: Taking your medications consistently shows the insurance company that you are stable and responsible, which helps me get you a better deal.

Some carriers have updated their internal rules to offer better immediate-coverage options for people with controlled autism. Most people will have no trouble qualifying for and affording an instant-approval policy if they can manage their own affairs.

Autism Medical Definition & Health Risks

Insurers classify the risk level of autism based on medical history and how the condition affects daily communication and social interaction. Because autism is a developmental condition, underwriters evaluate independent living skills and steady employment to determine your final insurance rate. Since it is not a progressive disease, your health profile stays relatively stable compared to someone with a physical illness.

However, poor control or a lack of independence can lead to secondary issues like social isolation or severe depression. Insurance companies focus on your ability to function because they want to ensure you can manage your health and your policy independently.

Life Insurance Companies Ask These Autism & Mental Health Questions

Different life insurance companies ask different questions to decide which applicants with autism or mental conditions they may approve.

- Aetna Decline – Do you use a wheelchair or mobility scooter, or do you have any physical or mental impairment requiring assistance from another person with activities of daily living such as taking medications, bathing, dressing, eating, toileting, getting in or out of bed or chair, or moving about?

- Aetna Decline – Have you ever been diagnosed with, received, or been advised to receive treatment or medication for alzheimer’s disease, dementia, or mental incapacity?

- Aflac Decline – Do you use a wheelchair or mobility scooter, or do you have any physical or mental impairment requiring assistance from another person with activities of daily living such as taking medications, bathing, dressing, eating, toileting, getting in or out of bed or chair, or moving about?

- Aflac Decline – Have you ever been diagnosed with, received, or been advised to receive treatment or medication for Alzheimer’s disease, dementia, or mental incapacity?

- CICA Life Level – Are you currently hospitalized, confined to a bed or nursing facility, residing in an assisted living facility, receiving hospice care, or do you have any physical or mental impairment for which you need or receive assistance or supervision in performing normal activities of daily living, unable to care for yourself, or terminally ill?

- CICA Life Level – Have you ever been medically diagnosed, treated by a member of the medical profession, or prescribed medication for mental disorder, disorder of the brain or nervous system, systemic lupus (SLE), Alzheimer’s disease, dementia, brain disease, organic brain syndrome, Lou Gehrig’s disease (ALS), Huntington’s disease, muscular dystrophy, cystic fibrosis, pulmonary fibrosis, or multiple myeloma?

- Family Benefit Life Decline – Have you ever been diagnosed by a medical professional for, or taken medication for, dementia, Alzheimer’s disease, mental incapacity, Down syndrome, Huntington’s disease, Lou Gehrig’s disease (ALS), cystic fibrosis, cerebral palsy, muscular dystrophy, or sickle cell anemia?

- Family Benefit Life Level – Have you ever been diagnosed as having multiple sclerosis, epilepsy, schizophrenia, Parkinson’s disease, nephropathy, neuropathy, retinopathy, chronic kidney disease or failure, systemic lupus, hepatitis B or C, cirrhosis of the liver, liver disease, liver failure, or lung impairments including chronic obstructive pulmonary disease (COPD), chronic asthma, chronic bronchitis, emphysema, or fibrosis?

- Guarantee Trust Life Graded – Are you CURRENTLY bedridden, confined to a hospital, nursing home, mental care facility, long term care facility, hospice or have you been diagnosed with an end-stage or terminal illness, or been told by a medical professional that you have less than 12 months to live?

- Liberty Bankers Life Decline – Have you, the Proposed Insured, ever been diagnosed, treated, tested positive for, or been given medical advice by a member of the medical profession for; organ transplant (other than corneal), bone marrow transplant, stem cell treatment, kidney failure or dialysis, muscular dystrophy, mental incapacity, amyotrophic lateral sclerosis (ALS) or Lou Gehrig’s disease, Down’s syndrome, cystic fibrosis, pulmonary fibrosis, or Huntington’s disease?

- Liberty Bankers Life Decline – Have you, by a member of the medical profession, within the prior 2 years, been diagnosed with, or received, or been advised to receive treatment or medication for uncontrolled diabetes, uncontrolled high blood pressure, a diabetic coma or insulin shock, amputation due to diabetic complications, schizophrenia, alcohol or drug abuse, illegal use of drugs, or dependency on prescription medication?

- Mutual of Omaha Decline – Has the Proposed Insured ever been diagnosed by a licensed medical professional with, received treatment by a licensed medical professional for, or been advised to seek treatment by a licensed medical professional for; Alzheimer’s Disease, Dementia, Huntington’s Disease, Sickle Cell Anemia, Myelodysplastic Syndrome (MDS), Lou Gehrig’s Disease (ALS), Hydrocephalus, Muscular Dystrophy, Quadriplegia, Paraplegia, Down Syndrome, Intellectual Developmental Disorder, Congestive Heart Failure, Cirrhosis, Metastatic Cancer or recurrent Cancer of the same type?

- Mutual of Omaha Level – In the past 2 years, has the Proposed Insured been hospitalized by a licensed medical professional for any mental or nervous disorder?

- Mutual of Omaha Level – In the past 4 years, has the Proposed Insured been diagnosed by a licensed medical professional with, received treatment by a licensed medical professional for, or been advised to seek treatment by a licensed medical professional for Bipolar Depression, Schizophrenia, Parkinson’s Disease or Multiple Sclerosis?

- Trinity Life Decline – Have you ever been diagnosed by a medical professional for, or taken medication for, dementia, Alzheimer’s disease, mental incapacity, Down syndrome, Huntington’s disease, Lou Gehrig’s disease (ALS), cystic fibrosis, cerebral palsy, muscular dystrophy, or sickle cell anemia?

- Trinity Life Level – Have you ever been diagnosed as having multiple sclerosis, epilepsy, schizophrenia, Parkinson’s disease, nephropathy, neuropathy, retinopathy, chronic kidney disease or failure, systemic lupus, hepatitis B or C, cirrhosis of the liver, liver disease, liver failure, or lung impairments including chronic obstructive pulmonary disease (COPD), chronic asthma, chronic bronchitis, emphysema, or fibrosis?

Autism Underwriting Basics

Independent living status proves your medical stability to the insurance company.

- Testing & Test Results: Underwriters look for a 24-month history without behavioral crises or emergency hospitalizations. They want to see that you are high-functioning and capable of maintaining a standard lifestyle.

- Common Medications: Consistent medication use reduces mortality risk for the insurance company.

Not all companies view medications negatively. Using the right medications actually reduces the insurance company’s mortality risk.

- Why it Matters: Your specific treatment history controls the price you pay every month. If you have been stable on the same regimen for years, I can usually get you the same low rates as any other healthy senior.

Autism Prescription Medication Classes

Specific medication categories help the life insurance underwriter assess the severity of behavioral symptoms.

- Antipsychotics: Meds like Risperdal or Abilify help with mood regulation and irritability.

- Stimulants: Common focus medications include Adderall or Ritalin.

- Anticonvulsants: These prescriptions manage potential seizure activities or epilepsy.

- Anti-anxiety Meds: Doctors often prescribe these for social anxiety or depression.

Autism with Comorbidities

Insurers evaluate how overlapping health profiles influence the total insurance risk for every applicant. If you have autism alongside epilepsy, the insurer will scrutinize your safety risk to determine if additional accidental death protections are necessary. Sleep disorders are also common and can lead to long-term strain on your heart or immune system if left untreated. Many people also deal with chronic anxiety or depression, which can affect your risk class if those conditions lead to self-harm or frequent hospital visits.

The most important message is that you need to lock in your protection now before a secondary diagnosis makes you harder to cover. Controlled autism allows for immediate level burial insurance coverage even with the most common secondary health issues.

Other Common Health Issues with Autism

Autism affects brain development and nervous system processing in ways that influence communication, behavior, and sensory regulation, and these related challenges can affect underwriting decisions and policy selection when they’re present.

- Communication difficulties – Delayed or limited speech and language processing affect social interaction, learning, and daily functioning.

- Sensory processing issues – Heightened or reduced sensitivity to sound, light, touch, or texture can cause distress and limit the environments a person can tolerate.

- Anxiety disorders – High rates of chronic anxiety lead to sleep disruption, avoidance behaviors, and reduced independence.

- Depression – Social isolation and ongoing stress increase depression risk, especially in adolescents and adults.

- Sleep disorders – Difficulty falling or staying asleep affects mood, attention, and daytime performance.

- Behavioral challenges – Repetitive behaviors, rigidity, and emotional dysregulation interfere with school, work, and relationships.

- Intellectual disability – Some individuals experience cognitive limitations that affect learning speed, reasoning, and independent living.

- ADHD symptoms – Inattention, impulsivity, and hyperactivity complicate focus, organization, and task completion.

- Seizure disorders – Epilepsy occurs more frequently and can affect safety, independence, and medical risk profiles.

- Gastrointestinal issues – Chronic constipation, diarrhea, or abdominal pain affect comfort, nutrition, and daily routines.

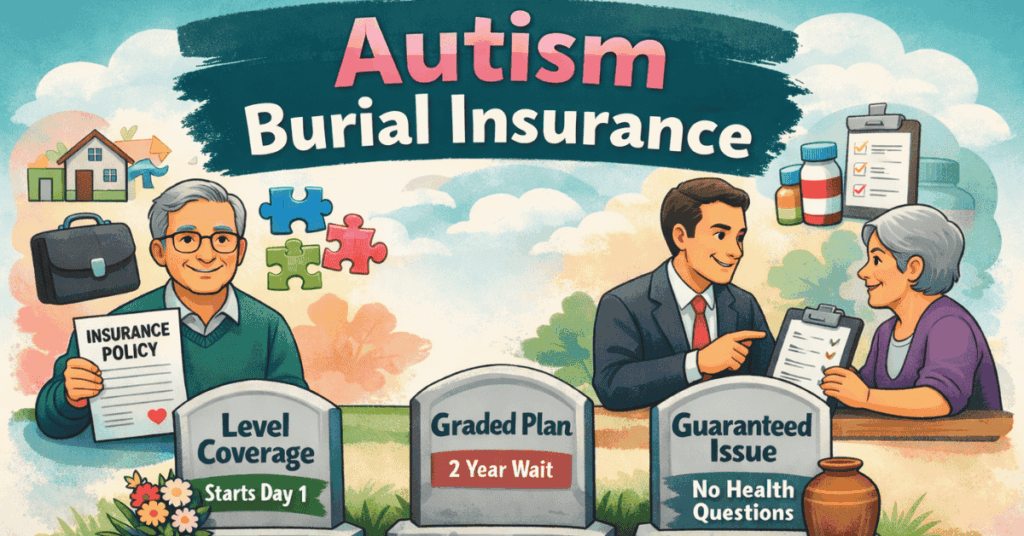

Understanding Autism Policy Types

Carriers offer different plan categories based on an applicant’s autism and long-term & short-term health stability.

- Level: Level burial insurance offers first-day coverage and pays the full death benefit from day 1. This is the goal for high-functioning people who live independently.

- Graded: Graded burial insurance limits benefits during the 12 to 24 months for health or medical-related causes of death. This is common if you have significant secondary issues like heart disease.

- Guaranteed Issue: Guaranteed issue burial insurance requires no health questions but includes a 2-year waiting period before it pays out for causes of death related to health or medical conditions. This acts as a safety net if you need help with daily hygiene.

Sample Autism Rate Snapshot for $10,000 Coverage

Insurers use age-based pricing to determine the direct cost of burial insurance premiums for every family. Monthly rates increase significantly as you age, so locking in a policy now secures the lowest possible price for the life of the plan. Women pay lower rates because they statistically live longer than men, but everyone benefits from locking in a rate early.

Here are some preferred rates, but your final cost depends on which A-rated carrier best fits your specific health profile.

AFLAC PREFERRED LIFE INSURANCE RATES AGE 50–80

| AGE | $10,000 | $15,000 | $20,000 | $25,000 |

|---|---|---|---|---|

| 50 | F: $26 M: $33 |

F: $38 M: $48 |

F: $49 M: $62 |

F: $61 M: $77 |

| 55 | F: $29 M: $38 |

F: $42 M: $55 |

F: $54 M: $72 |

F: $67 M: $89 |

| 60 | F: $34 M: $45 |

F: $49 M: $65 |

F: $65 M: $86 |

F: $80 M: $106 |

| 65 | F: $43 M: $55 |

F: $63 M: $81 |

F: $63 M: $107 |

F: $103 M: $133 |

| 70 | F: $55 M: $71 |

F: $81 M: $105 |

F: $107 M: $139 |

F: $133 M: $173 |

| 75 | F: $81 M: $97 |

F: $120 M: $147 |

F: $159 M: $195 |

F: $198 M: $243 |

| 80 | F: $115 M: $155 |

F: $171 M: $231 |

F: $227 M: $307 |

F: $283 M: $383 |

Rates may vary based on age, gender, health, and state. Click the form on this page for the lowest rates from the best carriers.

Autism Underwriting & Medication History

Insurers use your prescription history to verify medical stability and confirm that you are managing your health effectively. Consistently following a treatment plan is a major positive sign that can help you qualify for better rate classes during the underwriting process. I can tell you that if you have been on the same stable medication for years, it proves you are a responsible risk. Carriers run a quick background check on your prescriptions to see if you are filling your meds regularly. Consistency shows me that you are high-functioning and deserve the best possible price.

Your prescription history is how the insurance carriers verify medical stability. Recent hospitalizations for crises trigger postponement rather than permanent decline.

| Health Profile | Coverage Type | Wait Period |

|---|---|---|

| High Functioning | Level (Day 1) | None |

| Comorbidity Issues | Graded | 2 Years |

| ADL Assistance Needed | Guaranteed Issue | 2 Years |

Real Life Autism Success Stories

Real-world examples illustrate how people with autism secure day-one protection with anywhere from $5,000 to $25,000 for burial and final expenses.

Robert’s Story

Robert was a 66-year-old man with high-functioning autism who worked as a librarian. He lived on his own and was fully capable, but he was terrified that his diagnosis would make insurance a total rip-off. I helped him apply for a preferred plan with Aflac, which accepted his independence and granted him first-day coverage. He secured a $12,000 policy to cover his burial costs and saved 20% compared to the mailers he had been receiving. Now his sister won’t have to foot the bill for his final wishes.

Susan’s Story

Susan was 62 and had autism along with some social heavy-duty heart medications. She was worried that her prescriptions would be a deal-breaker for most companies. I placed her with Guarantee Trust Life because they are forgiving of this developmental condition. She was approved for a $10,000 policy that starts on day 1 with no waiting period. Susan was thrilled to find a plan that respected her lifestyle and stayed within her monthly budget.

Financial Ratings & Stability

Insurers use financial ratings to verify a carrier’s ability to pay death claims when your family needs them. Buying a policy from a weak company is risky because they may lack the capital to fulfill long-term obligations decades from now. You need a carrier with high A.M. Best ratings to ensure they have the cash to pay your family in 20 years.

I also check the BBB to make sure they don’t make beneficiaries jump through hoops during a difficult time. You want a company that pays out in days, not months.

Insurance Carrier Ratings & Comparisons

| Carrier | A.M. Best | BBB | NAIC Complaints |

|---|---|---|---|

| Aflac | A+ (Superior) | A+ | Low |

| CICA | B++ (Good) | A+ | Low |

| Colonial Penn | A (Excellent) | A+ | High (300% Above Avg) |

| Family Benefit Life | A+ (Superior) | A+ | Low |

| Guarantee Trust Life | A (Excellent) | A+ | Low |

| Senior Life | Not Rated | A+ | High (300% Above Avg) |

| Trinity Life | A+ (Superior) | A+ | Low |

Frequently Asked Questions: Autism Burial Insurance

Can you get burial insurance if you have autism?

Most final expense insurance companies approve applicants with autism because the condition is not included on their standard health checklists. Many families mistakenly believe that an autism diagnosis acts as a total deal-breaker. Honestly, it just does not make sense to worry about it when the carriers care more about your heart and lungs than how your brain is wired. This allows you to secure a policy that treats you exactly like anyone else in your neighborhood. Since the companies ignore the diagnosis, you avoid the high prices that usually come with special medical conditions.

Does autism count as a “pre-existing condition” for burial insurance?

Insurance underwriters view autism as a stable health history rather than a life-threatening risk that would impact your family’s coverage. Yes, it is technically a pre-existing condition, but do not let that corporate talk scare you away from protecting your family. Unlike heart disease or cancer, underwriters do not think autism will shorten your life. A stable medical history ensures you get the best deal available today. Unless you have a severe cognitive impairment that stops you from signing a contract, the insurance company will treat you as a standard applicant.

Is immediate burial insurance coverage available for autistic adults?

Autistic adults qualify for first-day coverage when they live independently or maintain a stable health history without major medical complications. You do not have to settle for a two-year waiting period just because you are on the spectrum. If you live independently or only need a little help with your daily routine, you can find first-day coverage today. It is like paying for a full gallon of milk: you get the full benefit immediately without any hidden delays or convenience taxes. This means your family receives the full protection of the policy from the very first premium payment.

Do insurance companies check for autism medications like Risperdal or Abilify?

The insurance company conducts a quick background check of your prescriptions to verify that you are consistently managing your health in line with your doctor’s plan. This check identifies what you are taking so you can pick the right company for your budget. Maintenance drugs do not block your ability to qualify for a great plan. If they see Risperdal or Abilify, they might ask a few questions, but they usually do not care about these specific meds. Taking your medication actually shows the underwriter that you are a responsible applicant, which helps secure your policy at a fair price.

Does being on Social Security Disability (SSDI) for autism affect burial insurance eligibility?

Insurance companies approve most applicants on SSDI because they prioritize your physical longevity over your current employment status. Hundreds of folks in fixed-income households get the coverage they need without any hassle. The insurance company cares about your physical health, not your job status or your disability check. While some picky plans might turn you away, standard plans welcome you with open arms. Every dollar saved on premiums is another dollar that stays in your pocket for your own daily needs.

What happens if an autistic person cannot legally sign the burial insurance contract?

Legal representatives cannot use Power of Attorney signatures to complete the application process. If a person cannot understand the contract, they should consider other ways to financially protect their loved ones. Proper planning prevents problems later.

Are there specific “autism-friendly” burial insurance companies?

Independent agents locate the best autism-friendly carriers that offer lenient underwriting for neurological conditions. Certain companies have a soft spot for neurological conditions and ignore the therapy notes that other companies might use against you. Framing your application correctly saves you from overpaying with the wrong company.