Stent Burial Insurance

Here’s the Bottom Line:

• A heart stent puts you in a higher-risk insurance category

• Applying within 6 to 12 months often leads to delays or denials

• Many people get pushed into expensive waiting period policies

• Multiple stents or a heart history can raise your monthly cost fast

• The wrong timing can cost you better coverage options

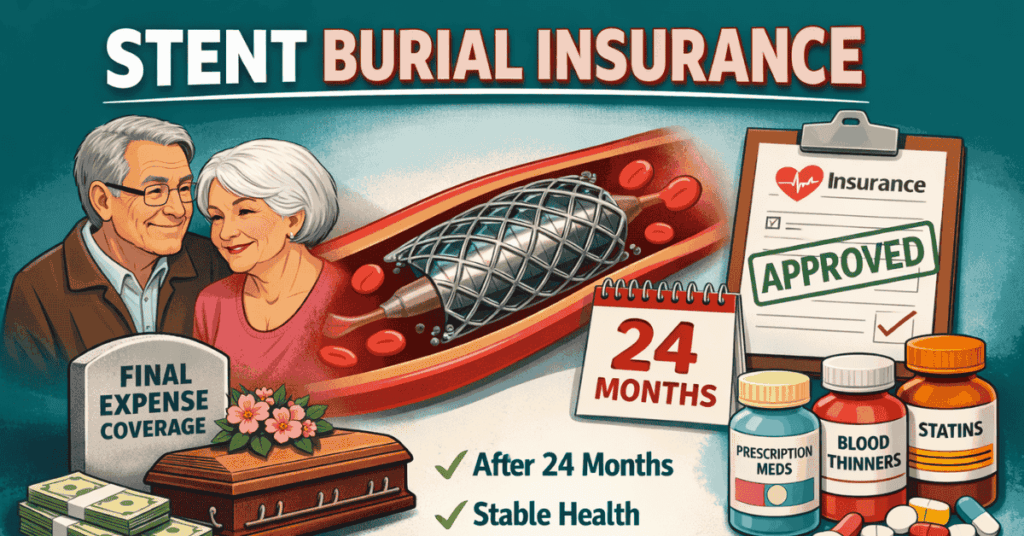

Getting burial insurance after a heart stent is very doable, but timing and recovery matter more than anything. Burial insurance is a type of whole life insurance designed to cover funeral and final expenses, even if you’ve had heart procedures. Most companies want to see at least 6 to 12 months of stable recovery before approving better plans, and applying too early can lead to higher costs or limited options. If your health is stable and well-managed, you may still qualify for first-day coverage instead of a 2-year waiting period policy.

Complete my quote request form on this page to quickly avoid choosing the wrong plan.

Stent Burial Insurance Insights

- The 24-month timeline: Reaching the 2-year milestone after your stent implant is generally the timeframe to get the lowest market rates and immediate full benefits. Most top-tier carriers use this window to transition you from high-cost plans to standard first-day coverage.

- Circulatory surgery rules: These guidelines apply directly to stent procedures. Insurers treat the implant date as a major milestone to determine your risk level and eligibility for them mostn competitive pricing.

- Pending procedures: Any unresolved medical actions will stop an approval for first-day coverage. All outstanding heart tests or consultations should be completed before applying to avoid an automatic decline.

- Stable medication use: Consistent use of prescribed medications demonstrates to the insurer that you are compliant with your treatments, and therefore a better candidate for first-day coverage.

- Carrier selection: Finding the right provider is the secret to securing day-one protection. CICA Life is often the best choice if your stent implant was within the last 24 months. Family Benefit Life, Trinity Life, and Aflac are the best choices after 24 months from your stent surgery date.

Stents are a big deal to many insurance companies, but I’m always on the lookout for companies that offer 1st-day coverage in the months after a stent implant.

Stent Medical Definition & Health Risks

Underwriters assess your stent risk based on how long it has been since the procedure and any recurring symptoms. Because insurance companies classify a stent as a form of circulatory or cardiovascular surgery, they use the time elapsed since the operation to decide if you qualify for immediate coverage. While the stent often resolves the immediate blockage, the underlying plaque or high cholesterol levels remain factors in your future health. If you do not manage these risks, you are more likely to need additional stents in other parts of your body later.

Life Insurance Companies Ask These Heart Stent Questions

Different life insurance companies ask different questions to decide which heart stent applicants they may approve.

- Aetna Decline – Have you ever been diagnosed with, received, or been advised to receive treatment or medication for congestive heart failure, pulmonary fibrosis, any terminal condition, or end-stage disease?

- Aetna Decline – Have you ever been diagnosed with, received, or been advised to receive treatment or medication for cerebral palsy, cystic fibrosis, muscular dystrophy, or un-operated heart defects?

- Aetna Modified – Within the past year, have you been diagnosed with, received, or been advised to receive treatment for angina (chest pain), heart attack, cardiomyopathy, or any type of heart or circulatory procedure or surgery?

- Aetna Level – Within the past 2 years, have you been diagnosed with, received, or been advised to receive treatment for angina (chest pain), heart attack, cardiomyopathy, or any type of heart or circulatory procedure or surgery?

- Aflac Decline – Have you ever been diagnosed with, received, or been advised to receive treatment or medication for congestive heart failure, pulmonary fibrosis, any terminal condition, or end-stage disease?

- Aflac Decline – Have you ever been diagnosed with, received, or been advised to receive treatment or medication for cerebral palsy, cystic fibrosis, muscular dystrophy, or un-operated heart defects?

- Aflac Modified – Within the past year, have you been diagnosed with, received, or been advised to receive treatment for angina (chest pain), heart attack, cardiomyopathy, or any type of heart or circulatory procedure or surgery?

- Aflac Standard – Within the past 2 years, have you been diagnosed with, received, or been advised to receive treatment for angina (chest pain), heart attack, cardiomyopathy, or any type of heart or circulatory procedure or surgery?

- CICA Life Level – In the past 10 years, have you opted to not seek treatment, have not taken medication, or have not followed the prescribed treatment plan following a medical diagnosis by a member of the medical profession for any one or more of the following: uncontrolled diabetes, uncontrolled high blood pressure, stroke or TIA, paralysis, congestive heart failure, heart disease, cardiomyopathy, lung disease including COPD (chronic obstructive pulmonary disease) or emphysema, liver cirrhosis or failure, kidney (renal) failure or insufficiency, or chronic kidney disease including dialysis?

- Family Benefit Life Decline – Have you ever been diagnosed by a medical professional with a terminal illness, end-stage disease, congestive heart failure, or cardiomyopathy?

- Family Benefit Life Decline – Within the past 12 months, have you been diagnosed by a medical professional for, or hospitalized for, a heart attack, stroke, transient ischemic attack (TIA), angina, aneurysm, or had cardiac or circulatory surgery of any kind to improve circulation to the heart or brain?

- Family Benefit Life Level – During the past 24 months, have you been diagnosed, treated, tested positive for, or given medical advice by a medical professional for a heart attack, stroke, transient ischemic attack (TIA), angina, aneurysm, or had cardiac or circulatory surgery of any kind such as a pacemaker, heart valve replacement, bypass, angioplasty, or stent implant to improve circulation to the heart or brain?

- Liberty Bankers Life Decline – Have you, the Proposed Insured, ever been diagnosed, treated, tested positive for, or been given medical advice by a member of the medical profession for; congestive heart failure (CHF), cardiomyopathy, memory loss, Alzheimer’s, senile dementia, dementia, heart defibrillator implant, 2 or more instances of internal cancer(s), or terminal illness (“terminal illness” means a disease or illness that is expected to result in death within 24 months)?

- Liberty Bankers Life Modified – Within the past 2 years have you, the Proposed Insured, been diagnosed, treated, tested positive for, or been given medical advice by a member of the medical profession for; angina (chest pain), any type of heart or circulatory surgery or disease, heart valve disorder, heart attack, or received a pacemaker or stent?

- Liberty Bankers Life Preferred – Have you, the Proposed Insured, by a member of the medical profession, ever been diagnosed with, or received, or been advised to receive treatment or medication for Chronic Obstructive Pulmonary Disease (COPD), chronic bronchitis, emphysema, irregular heartbeat, atrial fibrillation, peripheral vascular disease or peripheral artery disease?

- Mutual of Omaha Decline – Has the Proposed Insured ever been diagnosed by a licensed medical professional with, received treatment by a licensed medical professional for, or been advised to seek treatment by a licensed medical professional for; Alzheimer’s Disease, Dementia, Huntington’s Disease, Sickle Cell Anemia, Myelodysplastic Syndrome (MDS), Lou Gehrig’s Disease (ALS), Hydrocephalus, Muscular Dystrophy, Quadriplegia, Paraplegia, Down Syndrome, Intellectual Developmental Disorder, Congestive Heart Failure, Cirrhosis, Metastatic Cancer or recurrent Cancer of the same type?

- Mutual of Omaha Decline – In the past 12 months, has the Proposed Insured been diagnosed by a licensed medical professional as having heart disease or heart surgery of any kind?

- Mutual of Omaha Level – In the past 2 years, has the Proposed Insured been diagnosed by a licensed medical professional with, received treatment by a licensed medical professional for, or been advised to seek treatment by a licensed medical professional for; Coronary Artery Disease, Heart Attack, Coronary Artery Bypass Surgery, Angioplasty, Cardiomyopathy, irregular heart rhythm, Pacemaker or Valvular Heart Disease with surgical repair or replacement?

- Trinity Life Level – Have you ever been diagnosed by a medical professional with a terminal illness, end-stage disease, congestive heart failure, or cardiomyopathy?

- Trinity Life Decline – Within the past 12 months, have you been diagnosed by a medical professional for, or hospitalized for, a heart attack, stroke, transient ischemic attack (TIA), angina, aneurysm, or had cardiac or circulatory surgery of any kind to improve circulation to the heart or brain?

- Trinity Life Level – During the past 24 months, have you been diagnosed, treated, tested positive for, or given medical advice by a medical professional for a heart attack, stroke, transient ischemic attack (TIA), angina, aneurysm, or had cardiac or circulatory surgery of any kind such as a pacemaker, heart valve replacement, bypass, angioplasty, or stent implant to improve circulation to the heart or brain?

Stent Underwriting Basics

Insurance companies check your heart stability to see if your “circulatory repair” was a permanent success.

- Testing & Test Results: Carriers look for pending tests or procedures. If you have an unresolved heart checkup, you are only eligible for a guaranteed-issue plan, so it is better to wait until those tests are complete to secure a better rate.

Medication stability over time reduces the insurance company’s perceived mortality risk, often allowing you to qualify for better coverage.

- Why it Matters: Showing the company that your stent procedure resolved the issue without complications helps me secure the best day-one coverage for you.

Stent Prescription Medication Classes

Your daily medications prove to the insurer that you are keeping your arteries open and your heart healthy.

- Antiplatelets: Plavix or Brilinta are used to prevent blood clots from forming inside the new stent mesh.

- Statins: Atorvastatin (Lipitor) is used to lower cholesterol and prevent new plaque buildup in your veins.

- Antihypertensives: Lisinopril or Metoprolol are used to help maintain a safe blood pressure for your heart.

Stent with Comorbidities

Insurance companies assess total risk by evaluating how a stent interacts with underlying conditions such as high blood pressure or metabolic disorders. Because these secondary issues may often be the cause of the initial blockage, underwriters evaluate the management of all your health factors together to determine your final premium rate. These conditions often lead to other health complications, so it is to your advantage to get insurance now while your health is stable. We can always reshop your policy later if your health improves, but securing a plan today protects your family from future price hikes if new issues arise.

With a controlled stent history, you will qualify for immediate burial insurance coverage from a single company (depending on your state), even with secondary health issues.

Other Common Health Issues With a Stent

A stent is placed to reopen a narrowed or blocked artery and restore blood flow, which improves circulation but also reflects underlying vascular disease, ongoing clotting, and heart risk that can affect underwriting and policy selection when these related issues are present.

- Underlying coronary artery disease – A stent treats a blockage but doesn’t reverse widespread plaque buildup that limits long-term heart health.

- Risk of restenosis: Scar tissue or new plaque can narrow the artery again, causing recurring symptoms.

- Blood clot risk – Stents increase clot risk when medication adherence is poor, raising heart attack or stroke risk.

- Medication dependence – Long-term antiplatelet therapy increases bleeding risk and affects medical stability.

- Chest pain recurrence – Angina can return if other arteries remain narrowed or the disease progresses.

- Exercise limitations – Heart disease can still limit endurance even after blood flow improves.

- Bleeding complications – Blood thinners raise the risk of bruising, gastrointestinal bleeding, or internal bleeding.

- Need for repeat procedures – Progressive disease may require additional stents or bypass surgery.

- Lifestyle restrictions – Ongoing diet, activity, and stress limits are often required to reduce recurrence.

- Reduced work reliability – Follow-up care, medication management, and symptom monitoring affect consistency and stamina.

Understanding Stent Policy Types

Carriers offer different plan categories based on an applicant’s Stent history and long-term health stability.

- Level: Level burial insurance offers 1st-day coverage and pays the full death benefit from day one. Trinity Life, Family Benefit Life, and Aflac are great choices for immediate coverage.

- Graded: Graded burial insurance limits benefits during the 12 to 24 months for health or medical-related causes of death. Gurantee Trust Life is a great graded plan for those with recent medical procedures.

- Guaranteed Issue: Guaranteed issue burial insurance requires no health questions but includes a 2-year waiting period before it pays out for causes of death related to health or medical conditions. Gerber Life is a great company for guaranteed coverage with no health questions.

Sample Stent Rate Snapshot for $10,000 Coverage

Age and gender are the primary factors in calculating burial insurance premiums because they define your statistical life expectancy. Women pay lower monthly rates than men because actuarial data show they live longer on average, meaning the insurance carrier expects to collect premiums over a longer period before paying a claim. It is a simple math fact that helps women save money on their monthly insurance bills.

Here are some preferred rates, but your rates can vary based on which A-rated carrier is best for your situation.

TRINITY LIFE & FAMILY BENEFIT INSURANCE RATES AGE 50–85

| AGE | $10,000 | $15,000 | $20,000 | $25,000 |

|---|---|---|---|---|

| 50 | F: $21 M: $27 | F: $31 M: $39 | F: $40 M: $52 | F: $50 M: $64 |

| 55 | F: $26 M: $32 | F: $38 M: $47 | F: $49 M: $62 | F: $61 M: $78 |

| 60 | F: $32 M: $41 | F: $47 M: $61 | F: $62 M: $80 | F: $77 M: $100 |

| 65 | F: $41 M: $53 | F: $60 M: $79 | F: $79 M: $104 | F: $99 M: $130 |

| 70 | F: $52 M: $69 | F: $76 M: $102 | F: $101 M: $135 | F: $126 M: $169 |

| 75 | F: $71 M: $96 | F: $106 M: $143 | F: $140 M: $190 | F: $175 M: $237 |

| 80 | F: $104 M: $145 | F: $155 M: $217 | F: $207 M: $288 | F: $258 M: $360 |

| 85 | F: $155 M: $192 | F: $231 M: $287 | F: $307 M: $382 | F: $384 M: $477 |

Rates may vary based on age, gender, health, and state. Click the form on this page for the lowest rates from the best carriers.

Stent Underwriting & Medication History

Underwriters use your prescription history to confirm that your health is stable and your heart condition is not worsening. Reaching the 24-month mark after a procedure or diagnosis is the primary milestone for unlocking the lowest insurance rates and immediate coverage. If your stent was placed more than 2 years ago, I can use top-tier companies like Family Benefit Life to secure first-day coverage. If you have had recent surgery, we look for companies like CICA Life that are more accommodating of recent circulatory procedures.

Your prescription history is how the insurance carriers verify medical stability. Recent hospitalizations for crises trigger postponement rather than permanent decline.

| Health Profile | Coverage Type | Wait Period |

|---|---|---|

| Stent Over 24 Months Ago | Level | None |

| Stent Within 24 Months | Level / Graded | Varies (0-2 Yrs) |

| Recurrent Chest Pain | Guaranteed Issue | 2 Years |

Real Life Stent Success Stories

Real-world examples illustrate how people with a Stent secure day-one protection with anywhere from $5,000 to $25,000 for their burial, cremation, or final expenses.

James’s Story

James had a stent surgery nearly three years ago and assumed he would be charged “high-risk” rates forever. Since he was past the 24-month mark and had no new chest pain, I placed him with Family Benefit Life for a $15,000 policy. James received first-day coverage and a rate that fit his fixed-income budget perfectly. He was relieved to know that his stents didn’t stop him from getting the same great deal as someone with no heart history. Now James can rest assured that his burial costs are fully covered.

Linda’s Story

Linda had a stent placed only 10 months ago and was told by other agents she had to wait two years for any payout. I helped her apply to CICA Life because they are more flexible regarding recent circulatory surgeries. Linda was approved for immediate first-day coverage, which was much better than the waiting-period plans she saw on TV. If her health had been worse, I could have used Guarantee Trust Life for a graded plan instead. Linda secured $10,000 for her cremation expenses and didn’t have to wait a single day for full protection.

Stent Financial Ratings & Stability

A.M. Best ratings serve as a financial report card, confirming that an insurance carrier maintains the necessary cash reserves to pay out death claims. A positive BBB history further validates the company, demonstrating that it handles customer service and claims processing with transparency and integrity. These ratings indicate the company has the financial strength to pay your claim promptly when your family needs it most. You shouldn’t gamble with a financially unstable company.

Insurance Carrier Ratings & Comparisons

| Carrier | A.M. Best | BBB | NAIC Complaints |

|---|---|---|---|

| Aflac | A+ (Superior) | A+ | Low |

| CICA | B++ (Good) | A+ | Low |

| Colonial Penn | A (Excellent) | A+ | High (300% Above Avg) |

| Family Benefit Life | A+ (Superior) | A+ | Low |

| Guarantee Trust Life | A (Excellent) | A+ | Low |

| Senior Life | Not Rated | A+ | High (300% Above Avg) |

| Trinity Life | A+ (Superior) | A+ | Low |

Frequently Asked Questions: Stent Burial Insurance

Can I get burial insurance if I have a heart condition?

Specialized burial insurance companies approve applicants with heart conditions every single day because these plans are built to handle seniors with a history of AFib, stents, or even past heart attacks. I have seen thousands of people assume their heart history makes them uninsurable, but honestly, it just does not make sense to walk away from protection when the market is this inclusive. These companies focus on your current stability rather than just your past medical charts. Most of these plans do not even require a medical exam, meaning you can secure permanent coverage with a few health questions and a quick background check on your prescriptions. I match your cardiac history with the right carrier so your family gets the check they need without any corporate red tape.

Is Day One burial insurance coverage available for people with heart issues?

Immediate first-day coverage is a realistic option for people with heart issues if your condition is medically managed and you are not currently in the hospital. Here is the part they do not tell you in the flashy TV commercials: many big-name insurers try to force every heart patient into a 2-year wait, but I know which carriers, like Family Benefit Life and Trinity Life, offer full protection starting on day 1. If you take your maintenance medications as prescribed, you can qualify for a level benefit plan that pays the full amount to your family even if you pass away shortly after the policy starts. This ensures your kids do not get stuck with a $15,000 funeral bill while waiting for a policy to take effect. You pay for immediate peace of mind, and that is exactly what I deliver.

What types of death are not covered by burial insurance?

Burial insurance covers almost all natural and accidental deaths, but it does include a few standard exclusions, like illegal activities or undisclosed extreme sports. The biggest exclusion you need to know about is the suicide clause, which typically states the company will not pay out if death by suicide occurs within the first 2 years of the policy. Other than that, once your policy is in force, your family is protected against heart attacks, strokes, accidents, or any other natural cause. Honestly, it just does not make sense to worry about the fine print when these policies are designed to be the simplest form of protection on the market. I ensure your plan is set up so your beneficiaries receive their money without a fight.

What is the difference between a level and a graded burial insurance policy?

A level policy provides 100% of your death benefit starting on the very first day, whereas a graded policy pays a partial amount for the first 24 months. If you have a recent or serious health event, a carrier might offer you a graded plan that pays out maybe 30% in the first year and 70% in the second year. But here is the kicker: after that 2-year period ends, the plan automatically becomes full coverage for the rest of your life. Graded plans are often a safety net for people who cannot qualify for a level plan today but want to start the clock on permanent protection. I help you understand the math so you know exactly what your family will receive and when.

Does AFib or Angina lead to higher burial insurance premiums?

AFib and angina do not necessarily lead to higher premiums if your symptoms are well-controlled with standard maintenance medications. Your monthly cost is primarily determined by your age and gender, and many carriers treat managed heart conditions as a standard risk. But if your heart issues are paired with serious complications like congestive heart failure, you might be moved into a higher-priced category. I shop your case across multiple carriers to find the one that does not penalize you for having a heart that beats a little differently. Every dollar we save on your premium is another dollar that stays in your pocket for your family’s future.

How do medications like blood thinners affect burial insurance qualification status?

Insurance companies view prescriptions for Eliquis or Plavix as a sign that you are a responsible patient actively managing your stroke and heart risk. Staying consistent with your blood thinners shows the underwriter that your health is under medical control, which makes it easier for you to qualify for first-day coverage. Honestly, it just does not make sense to hide your medications when they are the very evidence that shows you are at a lower risk for a sudden event. I perform a quick background check on your prescriptions to verify your stability and secure the best possible rate class for your policy. These drugs are a green light for many of my top-rated carriers.

Can I get burial insurance if I am waiting for heart surgery?

Insurance companies will postpone your application if you have a surgery or a major heart test currently scheduled because underwriters cannot assess your risk until the results are known. Whether it is a stent placement or a valve repair, the company wants to wait until the procedure is finished and your doctor confirms you are stable in a follow-up visit. Honestly, it just doesn’t make sense to apply while you are in “medical limbo,” because the company will just tell you to come back later. I recommend we wait until you have that clean post-op report. Once your health has stabilized, I can move fast to get your application approved, so your family has the protection they deserve.

Do I have to pay taxes on burial insurance proceeds?

The money your family receives from a burial insurance policy is generally exempt from federal income tax under current IRS rules. Unlike a 401(k) or an IRA, the death benefit is not considered gross income, so your spouse or kids get to keep every single dollar of the payout. This provides them with immediate financial relief to cover the funeral, pay off last bills, or handle any other debts you leave behind. I help you set up the policy so the cash goes directly to your beneficiaries without any tax headaches or red tape. It is a clean, simple wealth transfer that protects your legacy.

Why is whole life burial insurance better than term for heart patients?

Whole life burial insurance is a better deal for heart patients because it is a permanent policy that never expires and features rates that never increase. Term insurance is a gamble: if the policy ends after 10 or 20 years and your health has declined, you will be left with no coverage and no way to get a new policy. But with a burial policy, you own the coverage for the rest of your life. It builds a small cash value and ensures a check is waiting for your family, no matter how long you live. You should never “rent” your life insurance when you can lock in a price today that stays the same until you are 100 years old.