Colonial Penn Actor Jonathan Lawson – Broken Trust

last updated on October 21, 2025

last updated on October 21, 2025Jonathan Lawson has become the face of Colonial Penn’s terribly expensive $9.95 life insurance plan.

He appears in nearly every commercial, wearing a Navy uniform, promising peace of mind to seniors who just want to protect their families.

The company counts on viewers believing Jonathan Lawson’s credibility rather than checking the numbers themselves. Once you do the math, you’ll see how little protection these policies from Jonathan Lawson actually provide.

WHO IS JONATHAN LAWSON FROM COLONIAL PENN?

Jonathan Lawson is not just an actor. He’s a full-time employee of Colonial Penn and a retired U.S. Navy veteran.

He appears in nearly every commercial for the company, introducing himself by name and promoting the $9.95 plan as “affordable, guaranteed, and easy.”

A wonderful lady once said to me in a light-hearted and joking way that Jonathan was a “naughty boy” for selling policies that actually hurt seniors financially.

Jonathan is not the devil; in fact, he’s probably an OK guy in person, but many seniors might feel he’s not exactly doing “God’s work” either by overcharging seniors and forcing a 2-year wait policy onto them!

The main reason Colonial Penn features him because viewers recognize him after seeing so many of his commercials. When the same person appears in every advertisement, it builds familiarity with the brand. That repetition creates consistency, even when the details of the product are never fully explained.

In each commercial, Lawson focuses on the surface of the offer, the $9.95 price, the lack of medical questions, and the idea of guaranteed acceptance.

What he does not mention is the most important part: the limited coverage per unit, the mandatory two-year waiting period, and how quickly the benefit drops as you age.

His role is to present the plan, not to explain it. That’s what leaves most people believing they’re buying up to $50,000 protection for $9.95, when in reality they’re paying for a policy that may only offer hundreds of dollars in coverage, and doesn’t cover natural causes for two full years.

Most seniors think they have first-day coverage, only to find out later that they don’t, which is a painful financial discovery for any family.

Remember: I’ve reviewed these same policies with clients who thought they were protected. Once we went through the fine print, they realized how bad this $9.95 plan coverage really is.

WHAT JONATHAN LAWSON’S COMMERCIALS PROMISE

Colonial Penn’s ads repeat one phrase over and over: “Coverage starts at just $9.95 per month.”

Most viewers assume that Jonathan Lawsons $9.95 plan buys $10,000, $20,000, or even $50,000 in coverage. Butt, t doesn’t!

That price buys one unit of coverage, which can be as little as $400 to $1,500 depending on your age and gender.

The older you are, the smaller the benefit. To get meaningful coverage, you’ll need LOTS of units which means your monthly rate could be in the hundreds of dollars, far beyond the $9.95 that Jonathan Lawson repeatedly proclaims.

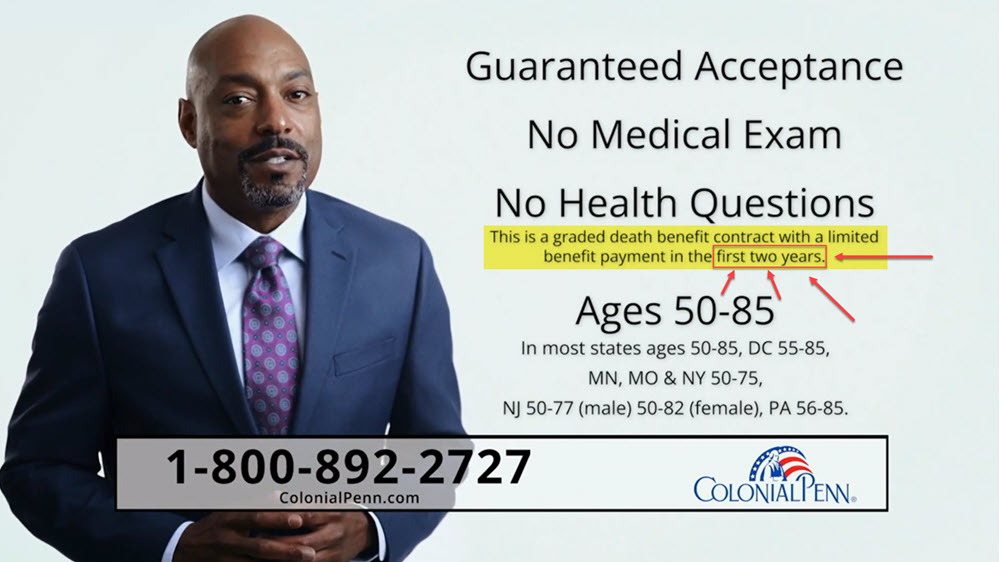

The commercials also say it’s “guaranteed acceptance,” meaning no health questions and no medical exam.

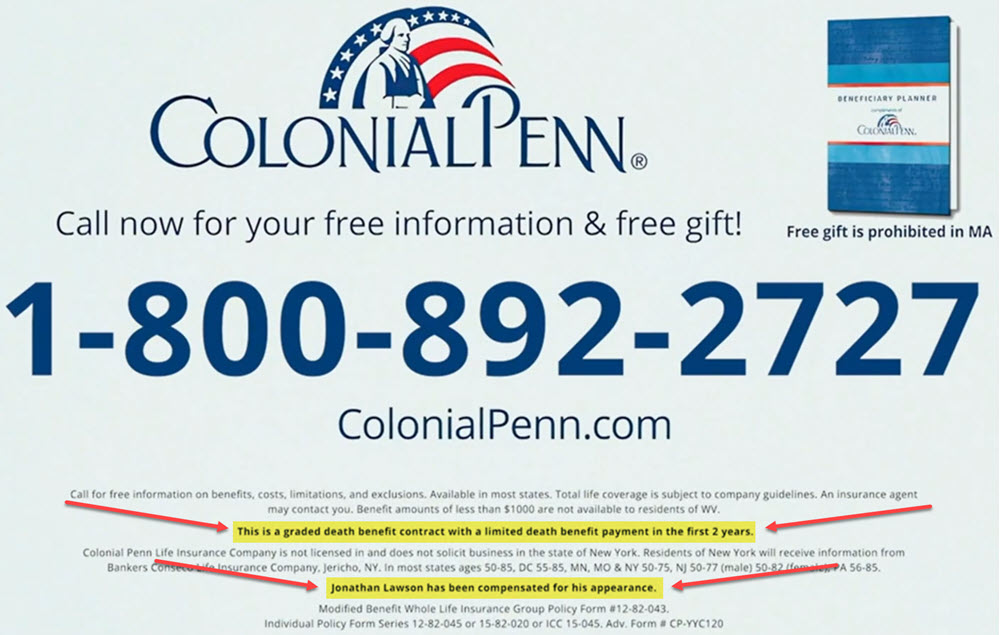

When an insurance company accepts everyone, it charges higher prices for everyone and limits coverage amounts to offset the risk. That’s why these plans include a MANDATORY two-year waiting period before paying any death benefit for natural causes.

That means you pay full premiums for two years before your loved ones can collect anything more than a refund plus interest.

Funeral Cost Percentage Breakdown

Jonathan Lawson knows that’s not true “protection from day one.” That’s essentially a refund plan sold as real insurance.

Jonathan’s TV ads never mention that. They never show the fine print on waiting periods or explain how coverage drops by age.

Remember: I’ve analyzed these commercials line by line. They’re carefully written to sound good while hiding the most important terrible facts about “guaranteed issue” life insurance coverage.

HOW MUCH DOES COLONIAL PENN PAY JONATHAN LAWSON?

Jonathan Lawson is the public face of Colonial Penn’s most profitable product, a guaranteed issue policy designed to generate massive revenue from small monthly payments that rarely result in real claims.

As the spokesperson and company employee, Lawson’s career depends on one thing: how many of these limited-benefit plans he helps sell.

His long-running commercial campaign has made Colonial Penn tens of millions of dollars each year by convincing seniors that $9.95 per month means they are getting $10,000, $20,000, or even $50,000, which is NEVER the truth.

Industry data shows that Colonial Penn spends over $60 million annually on television advertising their 2-year waiting period plan.

Colonial Penn and Jonathan Lawson would never approve spending that much unless those TV commercials were bringing in huge amounts of money from unsuspecting seniors.

It’s been reported that Jonathan Lawson earns up to or over $400,000 a year as their TV pitchman.

The terrible thing with the 995 plan is that the people with the least amount of money are funding those profits, and Jonathan Lawson’s lavish lifestyle.

Many of the people considering Colonial Penn are in such poor health that it makes them more likely to die during the two-year waiting period.

That means the company collects full premiums from the people least likely to receive a full payout.

From a financial standpoint, that’s brilliant marketing. From a consumer needs standpoint, that’s enough to make you lose your faith in the life insurance industry.

Jonathan Lawson’s commercials never mention that up to 97% of people could easily qualify for simplified issue whole life coverage, which starts immediately and costs far less than what the Final Expense Guy offers.

Many seniors say it’s difficult to reconcile Jonathan Lawson’s image with the sub-standard product he’s selling.

Every time a commercial airs, Lawson gets paid. Every time someone buys a $9.95 plan, Colonial Penn earns recurring premium revenue. Every time a policyholder dies within the 2-year waiting period, the company keeps those profits and pays back only a fraction.

That’s the Colonial Penn and Jonathan Lawson business model, and it’s why these commercials never stop running.

Remember: Lawson’s ads are designed to make you think it’s a great deal, even though it’s not.

HOW COLONIAL PENN’S $9.95 PLAN REALLY WORKS

Colonial Penn’s $9.95 plan is a guaranteed acceptance whole life policy with a 2-year waiting period.

That means anyone between the ages of 50 and 85 can qualify, no health questions asked.

The polices Jonathan Lawnon sells all have a MANDATORY two-year waiting period if you die of of any medical reason.

During those two years, if you pass away from an illness or health condition, your family doesn’t get the death benefit. They only receive the premiums you paid plus a small amount of interest, usually around 7%.

Only accidental deaths are paid in full during the first two years. Every other kind of death gets a MANDATORY two-year wait. That’s the part missing from every Jonathan Lawson commercial.

Colonial Penn and Jonathaan Lawson promote “peace of mind,” but a refund of premiums isn’t peace of mind. It’s reimbursement. Real-life insurance should provide protection from day one, not years later.

Then comes the biggest deception, the small amount of coverage per unit!

The $9.95 number they advertise on TV is for only one unit of coverage, not an actual dollar amount in terms of coverage.

One unit for a 50-year-old male might buy around $1,669 in protection. For a 70-year-old woman, that same $9.95 may only buy about $1,000.

To reach a realistic funeral cost of $10,000, you’d need seven to fifteen units, which means you could be paying up to or over $200 per month.

Once people learn this, they realize $9.95 was never a real price for real coverage; it was a deceptive advertising trick played on them by Jonathan Lawson and Colonial Penn.

These 2-year waiting period plans are called “guaranteed issue” policies. They’re meant for people in absolutely terrible health who can’t qualify for anything else.

About 97% of the people I help at the Final Expense Guy qualify for a simplified issue whole life policy with first-day coverage, with no waiting period, and much more coverage left behind for their loved ones.

Remember: I’ve helped thousands of seniors switch from refund-style plans to real protection, saving them money and giving their families peace of mind that actually starts day one.

JONATHAN LAWSON’S COMMERCIALS MISLEAD

Let me start by saying that Colonial Penn isn’t a scam, but lots of seniors do feel scammed by Jonathan Lawson and Colonial Penn.

Colonial Penn is a legitimate insurance company owned by CNO Financial Group, a publicly traded company. They use selective truth, which means accurate words are arranged to create a false impression.

Jonathan Lawson never lies directly when he’s talking on the TV.

He says, “You can get coverage starting at just $9.95 a month.” That’s true. But he doesn’t say how little coverage that $9.95 will purchase.

He says, “Guaranteed acceptance with no health questions.” Also true. But he doesn’t mention the 2-year waiting period that will leave your family unprotected for two years.

The ads focus on how easy it is to qualify, not what you actually get for your money.

An honest ad would say: “Coverage starts at $9.95 per unit, you’ll probably need LOTS of units, benefits vary by age, and policies have a mandatory 2-year waiting period.”

That’s the truth. But with policies as bad as the $9.95 plan, the truth doesn’t sell as well as intentional deception.

Remember: I’ve reviewed thousands of policies, and the fine print always tells a different story than the commercial does.

HOW MUCH COVERAGE DO YOU GET FOR $9.95?

When Colonial Penn and Jonathan Lawson say “$9.95 per month,” they’re talking about a confusing unit-based pricing system.

Many seniors say that once they find out the details, it feels like they are getting scammed.

The older you are, the less total benefits you receive for the same amount of money. That’s why two people paying $9.95 a month can have wildly different payouts.

Below is a clear example of what one unit of coverage looks like using Colonial Penn’s actual rate model:

| Age | Gender | Coverage for $9.95 (1 Unit) | Monthly Cost for $10,000 Coverage | Waiting Period |

|---|---|---|---|---|

| 50 | Male | $1,357 | $73 | 2 Years |

| 60 | Female | $932 | $107 | 2 Years |

| 70 | Male | $717 | $139 | 2 Years |

| 80 | Female | $426 | $234 | 2 Years |

Jonathan Lawson never tells you on the TV commercials that you’ll need multiple “units” to reach a helpful amount of funeral protection, and each additional unit costs another $9.95 per month.

For example, a 70-year-old man wanting $10,000 in coverage would pay nearly $139.30 monthly for a policy that doesn’t fully protect him until year three.

| Age | Male Coverage |

Female Coverage |

|---|---|---|

| 50 | $1,669 | $2,000 |

| 51 | $1,620 | $1,942 |

| 52 | $1,565 | $1,890 |

| 53 | $1,515 | $1,845 |

| 54 | $1,460 | $1,802 |

| 55 | $1,420 | $1,761 |

| 56 | $1,370 | $1,719 |

| 57 | $1,313 | $1,669 |

| 58 | $1,258 | $1,620 |

| 59 | $1,200 | $1,565 |

| 60 | $1,167 | $1,515 |

| 61 | $1,112 | $1,460 |

| 62 | $1,057 | $1,420 |

| 63 | $1,000 | $1,370 |

| 64 | $949 | $1,313 |

| 65 | $896 | $1,258 |

| 66 | $846 | $1,200 |

| 67 | $802 | $1,167 |

| 68 | $762 | $1,112 |

| 69 | $724 | $1,057 |

| 70 | $689 | $1,000 |

| 71 | $657 | $949 |

| 72 | $627 | $896 |

| 73 | $608 | $845 |

| 74 | $578 | $802 |

| 75 | $550 | $762 |

| 76 | $521 | $724 |

| 77 | $493 | $689 |

| 78 | $468 | $657 |

| 79 | $448 | $627 |

| 80 | $426 | $608 |

It’s one of the oldest marketing tactics in the world. Someone uses small numbers that sound affordable, and then tries to upsell you once they have you on the phone, and if that doesn’t work, then they quietly shrink your policy’s death benefit.

Remember: I’ve run these comparisons with real clients on an almost daily basis. The numbers don’t lie, even when Jonathan Lawson tries to distract you from the real numbers and costs.

COLONIAL PENN COMPLAINTS & FINANCIAL INFO

Colonial Penn is owned by CNO Financial Group, the same parent company that owns Bankers Life and Washington National.

Financially, CNO holds a stable A- rating from A.M. Best, which indicates good financial strength and the ability to pay claims. That’s not the issue.

The issue is consumer experience.

According to the National Association of Insurance Commissioners (NAIC), Colonial Penn consistently receives a higher-than-average number of complaints compared to other life insurers its size. Most of those complaints involve misleading advertising, slow claim processing, and misunderstanding of policy benefits.

The Better Business Bureau (BBB) lists similar patterns, including dozens of complaints from seniors who believed they had full coverage from day one, only to discover the two-year waiting period later.

Financial strength doesn’t protect you from Colonial Penn and Jonathan Lawson’s bad marketing. You can have an A- rating and still sell uninformed seniors the most overpriced limited-benefit policies in the country.

Remember: I check carrier ratings, complaint data, and claim records before I ever recommend a plan. That’s the difference between what looks safe and what actually is.

ALTERNATIVES TO COLONIAL PENN’S $9.95 PLAN

If your health is in good to moderately poor shape, you should never settle for a guaranteed issue plan from Colonial Penn or Jonathan Lawson.

Most people can qualify for simplified issue whole life insurance that starts immediately, with no waiting period and much higher coverage amount.

Simplified issue plans still skip medical exams but include a few health questions. That’s what keeps premiums lower and benefits higher.

It’s also how better companies honor their promise not to overcharge people in better health for coverage they don’t need.

Here’s a comparison showing how real first-day coverage stacks up against Jonathan Lawson and Colonial Penn’s $9.95 plan:

| Plan Type | Coverage Start | Health Questions | Average Monthly Cost (Age 65, $10K Benefit) | Benefit Type |

|---|---|---|---|---|

| Colonial Penn $9.95 (Guaranteed Issue) | After 2 Years | None | $108 | Refund + Interest First 2 Years |

| Simplified Issue Whole Life (First-Day Coverage) | Immediate | Yes, 5–10 Questions | $57 | Full Benefit Day One |

| Level Whole Life with Top A-Rated Carrier | Immediate | Yes | $51 | Full Benefit Day One |

This is why working with a licensed independent agent from the Final Expense Guy matters.

We compare dozens of reputable companies to find first-day coverage that fits both your health and budget, so you don’t have to overpay or wait two years just to qualify.

Some of the most trusted carriers offer better rates and stronger benefits than Colonial Penn, and they don’t rely on deceptive Jonathan Lawson TV ads to win customers.

These companies focus on value, not scam-like gimmicks.

Remember: I help families qualify for first-day coverage every week. The right plan should protect your loved ones from day one, not make them wait and hope for a refund.

HOW JONATHAN LAWSON’S ADS MISLEAD SENIORS

Jonathan Lawson’s commercials work because they blend trust, emotion, and half-truths.

The commercials intentionally leave out critical facts that every buyer deserves to know, like the MANDATORY two-year waiting period and the shrinking coverage value with age.

Colonial Penn’s marketing isn’t illegal, but it is deceptive by omission. The $9.95 hook is one of the most misleading price points in the entire insurance industry.

It’s not that Jonathan Lawson is lying, it’s just that he’s not telling the whole truth while on TV.

If you’re paying for life insurance, you should get protection now, not a refund later. And that’s exactly why first-day coverage is the standard among professionals who care about their clients and prospective clients.

When I help a client, I always ask: What do you need? What can you afford? What plan gives the best value right away and the most peace of mind?

That’s the difference between getting helped and getting taken advantage of.

Remember: I’ve helped thousands of families switch out of misleading plans and into coverage that actually pays when it matters most…from the very first day.

FREQUENTLY ASKED QUESTIONS: JONATHAN LAWSON – COLONIAL PENN

Who is Jonathan Lawson from Colonial Penn?

Jonathan Lawson is the spokesperson for Colonial Penn Life Insurance. He’s a real employee of the company and a retired U.S. Navy veteran. Colonial Penn uses him in commercials to connect with seniors who value trust, service, and discipline.

Does Jonathan actually work for Colonial Penn?

Yes. Unlike the previous spokespersons who were actors, Jonathan Lawson is a full-time employee. He works in their sales and marketing department and has appeared in ads for more than a decade.

Was Jonathan Lawson a Marine?

No. Jonathan Lawson served in the United States Navy, not the Marine Corps. His veteran background is part of why Colonial Penn features him in commercials – it builds credibility with viewers who respect military service.

How long has Jonathan Lawson been doing Colonial Penn commercials?

He began appearing in Colonial Penn ads around 2018 after the passing of Alex Trebek. Since then, he’s become the face of the company’s $9.95 guaranteed acceptance plan.

How much does Jonathan Lawson make from Colonial Penn?

His exact salary isn’t public, but as a corporate employee and spokesperson for a national insurance brand, he likely earns between $75,000 and $150,000 a year based on industry averages for media representatives.

How much is Jonathan from Colonial Penn worth?

Reliable estimates place his net worth between $300,000 and $500,000, mostly from his salary and long-term employment at Colonial Penn. These numbers are speculative, not verified.

Does Colonial Penn ever pay out?

Yes, Colonial Penn does pay claims. The problem is their most-advertised policy is a two-year waiting period plan. If someone dies of natural causes within those two years, the family only receives premiums paid plus interest – not the full death benefit.

What’s the gimmick with Colonial Penn life insurance?

The gimmick is the “$9.95 per unit” marketing. Each unit covers only a few hundred dollars of benefit depending on your age and gender. Most people would need several units, costing far more than advertised, to get meaningful coverage.

What are the drawbacks of Colonial Penn life insurance?

The drawbacks are low coverage, high cost per benefit dollar, and the two-year waiting period. For 97% of people, better options exist that offer first-day coverage at lower prices.

Is Jonathan Lawson really an employee of Colonial Penn?

Yes, he is. He’s not an actor or celebrity hire. Lawson has worked in marketing and customer service with Colonial Penn for many years.

Is Jonathan Lawson his real name?

Yes. His full name is Jonathan Lawson, and he publicly represents Colonial Penn in both TV and online advertising.

Is Jonathan Lawson married?

Jonathan keeps his personal life private, and Colonial Penn’s marketing focuses entirely on his role as a spokesperson, not his family background.

What did Jonathan Lawson do before Colonial Penn?

Before joining Colonial Penn, Lawson served in the U.S. Navy for 14 years. After leaving active duty, he began working in insurance and customer service before eventually becoming the company’s public face.

How old is Jonathan Lawson from Colonial Penn?

He’s believed to be in his early to mid-40s based on his service record and professional history. His exact age isn’t confirmed publicly.

How much does Colonial Penn pay Jonathan Lawson?

Colonial Penn hasn’t released his salary, but national advertising representatives for insurance companies typically earn six figures when including bonuses and sponsorship appearances.

What’s the income of Jonathan Lawson?

His estimated annual income is between $75,000 and $150,000 depending on salary and potential marketing bonuses. Again, that’s an educated estimate based on his position, not official disclosure.