Life Insurance Height and Weight Guidelines

last updated on December 15, 2025

last updated on December 15, 2025If you have no clue about “build charts” or minimum and maximum height & weight, life insurance can feel like it is full of complexities. Since maximums and minimums play such a huge part in getting your premiums, and/or getting approved, you should know about them.

In this article, I will share what height & weight charts (or build charts) are, how they work, what people complain about, what’s good, what’s bad, and what you can even do about it.

I hope you will see how consulting (or working) with a person like the Final Expense Guy can really help get you better rates and maybe even much more trustworthy help.

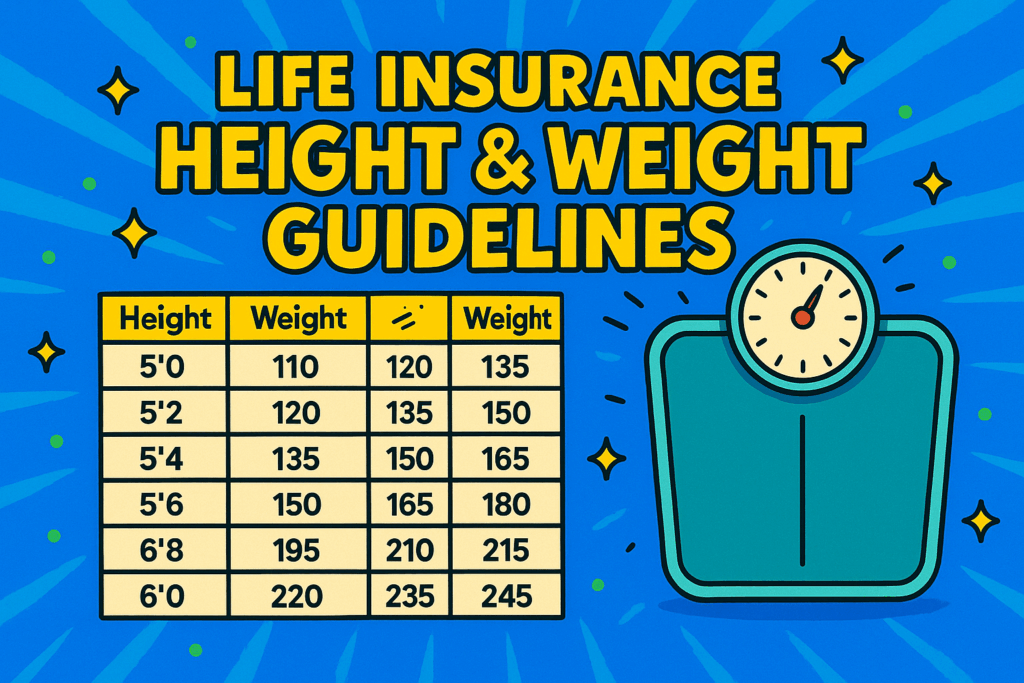

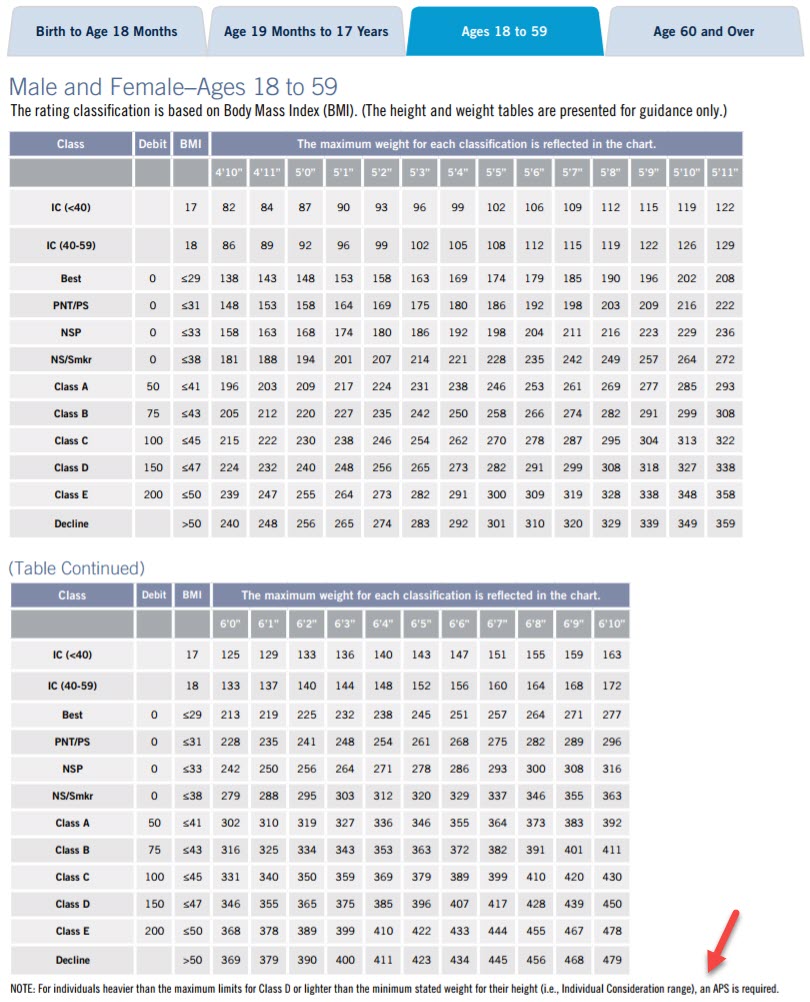

WHAT IS A BUILD CHART FOR LIFE INSURANCE?

A “Build Chart” is a height and weight chart used by an insurance company or life insurance agents to underwrite and identify what rate and health category you may fall into based on your height and weight only.

- If your height and weight fall within their optimum requirements based on your gender (and age in some cases), you can potentially get the lower rates from better insurance companies.

- If your height and weight are above or below their optimum requirements, you may still qualify for coverage, possibly just at a higher price. And if you go well over or under their chart requirements, you may be denied coverage with some companies, but not others.

- Some life insurance companies are stricter than others, and some companies will allow a wider margin to older applicants or those with good health metrics in other areas, such as cholesterol or blood pressure.

Bonus: This often seems complicated because no single chart is used for all insurance companies. Each insurance company has its own version (view some examples at the end of this article). The Final Expense Guy can get you set up with the best company based on your height and weight.

COMMON COMPLAINTS WITH LIFE INSURANCE BUILD CHARTS

Below are some of the most common complaints or concerns about “build charts”:

Charts Are Not Easily Accessible To The Public

Most insurers do not publicly provide their build charts. Until an applicant submits an application or sees the results of his or her medical exam, they do not know where the limits are. This can be a shock.

An applicant often does not know they will be penalized until either they apply to the insurer or have an agent (sometimes new or poorly trained, but usually just uneducated) tell them they can apply to a preferred class, only to find out they are marginally just above or below the weight.

BMI/Weight Misclassifies Muscular Or Abnormal Body Compositions

When relying on a BMI or height-weight chart, there is a potential misclassification if an applicant has a muscular build, a low percentage of body fat, and is generally healthy and at an appropriate height.

Some people worry about if BMI and/or charts will discriminate against muscular individuals and not against fat healthy individuals. Someone who lifts weights, runs, or even has lots of muscle mass can occasionally fall into an “overweight” or “obese” rating, even though they are not overweight.

Frustratingly, these build charts do not take into account muscle composition; they only take into account pounds.

Weight History May Be Considered

If applicants have a weight history, some insurers factor in your weight history.

If you have lost weight in the last 12-24 months, some companies will factor in any recent weight loss. If you lost 100 lbs in the previous 12 months, some companies may add 50 pounds of that onto your current weight, since they know that many people do eventually put some lost weight back on.

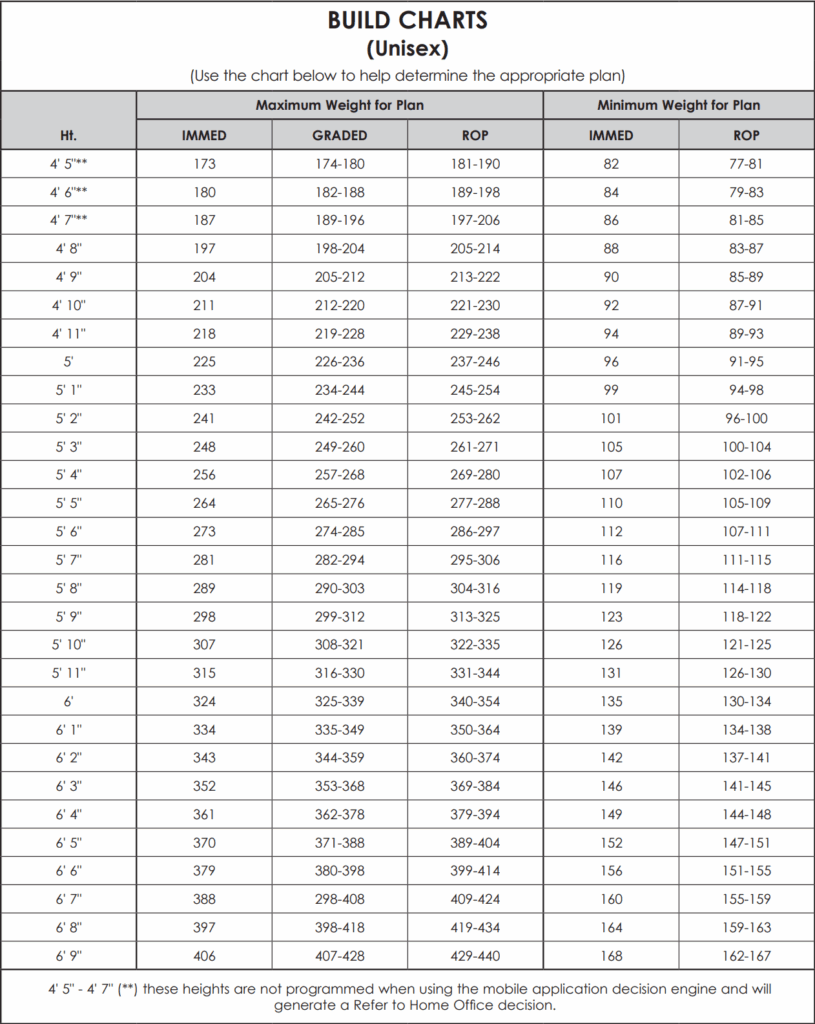

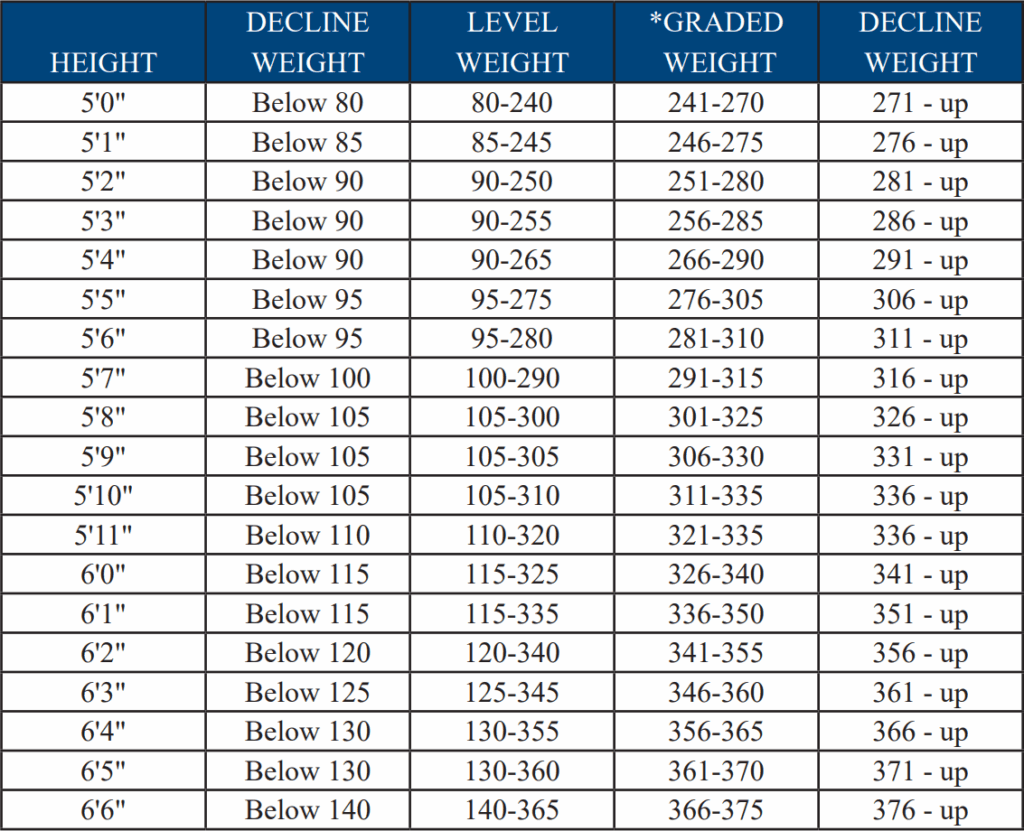

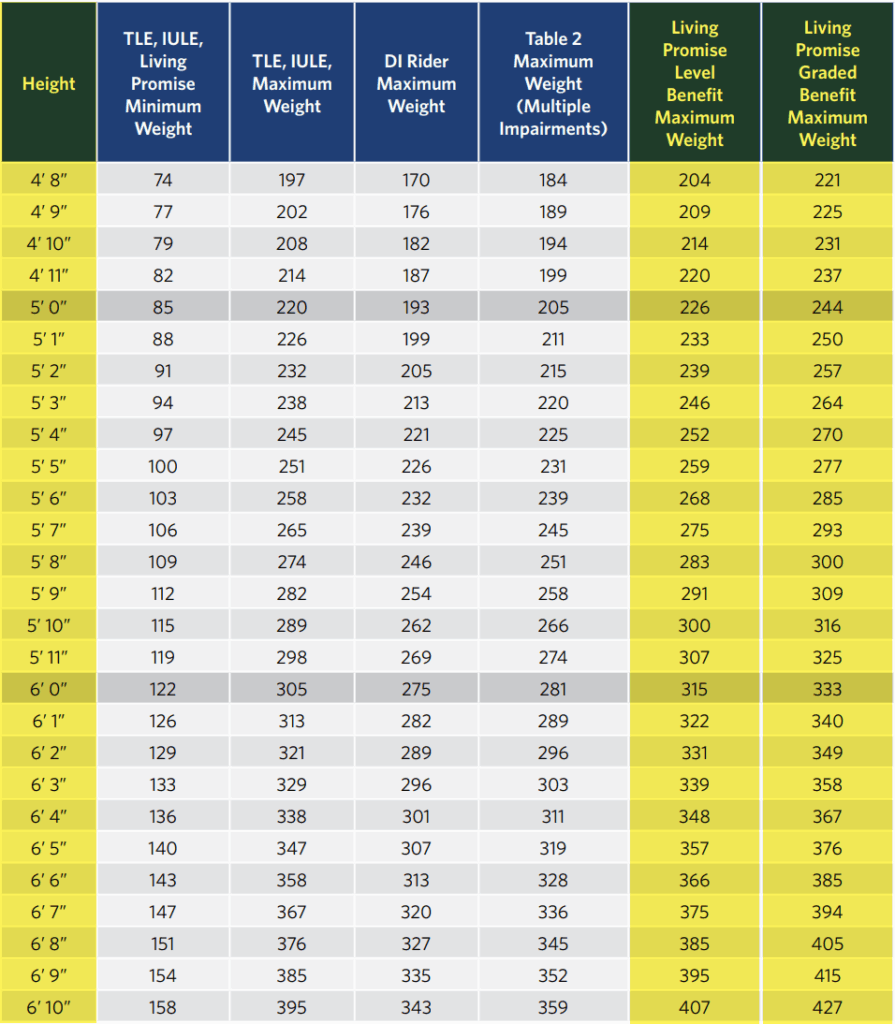

Charts Vary Significantly When Submitted

What one insurer considers “standard,” another will consider “substandard,” or even declines, which means an exchange with a knowledgeable broker/insurance agent is essential. Many consumers find that one insurer may decline them and another insurer approves, but at significantly different costs.

Being Underweight Also Assists

It’s not just being “too heavy” either. If you’re too light for your height, many insurers would also consider this part of a medical history risk. Being petite can also impact your future life insurance with some companies!

Underwriting Policies Differ Tremendously

Some companies have lenient guidelines, but other companies have guidelines and reject or heavily rate if the applicant is over or under specific weight restrictions. Some people are shocked by their lab results that classify them as “high risk.”

Bonus: When you work with a broker like the Final Expense Guy, you set yourself up for the best rates and the greatest amount of coverage.

WHY INSURERS USE BUILD CHARTS

Insurance companies using build charts for life insurance is a decades-old practice.

The insurance companies created these charts because they know that certain health factors, like being underweight or overweight, can influence mortality rates.

Being too far above or below average is almost always indicative of problems associated with specific health problems.

More companies are now offering “simplified issue” or “no medical exam” guidelines, which often do not include strict build charts or provide more flexibility (at a higher price or other qualifications). Many insurance applicants prefer these options, especially in situations where build charts result in policies that are too costly or would result in a decline.

Bonus: There are options for almost every height and weight. When you check with the Final Expense Guy, he’ll make sure you get the best deal.

PROS & CONS OF LIFE INSURANCE BUILD CHARTS

From the insurer’s perspective, using a height and weight chart adds consistency and predictability to the underwriting process. They standardize risk assessment so that those with similar health risks are underwritten in a similar way.

This provides a way for insurance companies to price fairly (from their standpoint) and limits arbitrary decisions.

From the insured’s perspective, this can be frustrating if they are over or under the build chart limits and are then charged more, or possibly declined for coverage.

A person may be subject to a rate class penalty because they are “over” a chart cutoff by just a couple of pounds, even though all other health metrics are well within normal ranges. This may feel unjust.

Also, using BMI or weight classifications can be misleading as charts don’t typically differentiate between fat, muscle, bone density, or body composition.

As an extreme example, a weight lifter or athlete could be rated in a lower class for having more muscle.

Bonus: If you are underweight or overweight, you need a broker like the Final Expense Guy who will shop your application with many different insurance companies so you can get the lowesnt rate and best coverage.

WHAT TO EXPECT MOVING FORWARD

There is a trend towards “simplified underwriting”.

There is growing availability for simplified issue and final expense insurance that is less strict or even has no height & weight chart limits. These can make for a solid backup option for anyone who struggles with strict build charts.

Insurance companies are also adapting and using alternative criteria, such as Body Mass Index (BMI), waist circumference, or laboratory data, instead of relying solely on weights measured on a scale.

Bonus: Some of these options are more appropriate than others for people whose height or weight would otherwise exclude them from coverage. It’s to your advantage to let the Final Expense Guy do the shopping for you.

WHAT IF YOU DON’T MEET THE CHART REQUIREMENTS?

Here are several strategies if you’re a bit out of the required “build chart” specifications:

Improve Your Health Metrics

If it’s medically safe, lose weight, reduce blood pressure, improve cholesterol, and improve blood sugar control. Even if you only have modest improvements, that may push you into a better rate class.

Wait And Stabilize Your Weight

Sometimes the underwriters want your weight to be stable for a few months. If you’ve recently lost weight, your medical history still counts. Sometimes waiting until your weight stabilizes can be beneficial before you apply.

Consider More Than One Insurance Company

Charts vary greatly in detail between carriers. Some are more forgiving. The Final Expense Guy can direct you to more forgiving or more favorable build charts, which can lead to better rates.

Consider Final Expense or Burial Insurance

These types of policies often have less strict build charts or may not have them at all.

Consider Guaranteed Issue or Simplified Issue Coverage

Companies offering guaranteed-issue polices don’t have any medical exams or ask any health questions. A simplified issue may not have all the medical requirements as a fully underwritten policy.

Fully Disclose Your Health History

Always be honest and upfront on your application. The underwriters will check your records for health or medical impairments. If they find out you have omitted specific details, it’s not going to benefit your application for coverage.

Seek Out Expert Or Broker Help

Any broker or agent who knows the insurance market can get you set up with a company with more forgiving build charts or better underwriting. The Final Expense Guy is an example of someone who can help anyone with weight/build challenges find better rates and competent help.

Bonus: You don’t have to decide on this today, but the Final Expense Guy recommends you at least look into your best options, and then decide what to do from there.

SUGGESTIONS FOR GETTING THE LOWEST LIFE INSURANCE RATES:

Here are a few suggestions to get working on if you know you’ll want some life insurance in the future:

- Start managing your cholesterol, blood pressure, and blood sugar levels even if you’re slightly over ideal weight. Don’t worry about getting off your medications, as these are a non-issue as long as you go with the right company the first time.

- Slowly and safely lose weight. New medical or health issues can occur from crash dieting, and the insurance company will often review your weight over the last 1-2 years, so crash dieting doesn’t fool the life insurance companies.

- Stop smoking. Non-smokers get much lower rates than smokers…because it helps you live longer. The insurance companies will often ask you how long you have smoked and how long it’s been since you quit.

- Also, be aware that many people put on weight after quitting smoking, so you may be better off applying at smoking rates rather than overweight rates.

WHY THE FINAL EXPENSE GUY

The Final Expense Guy shops multiple carriers to find the best match for height, weight, and general health.

Instead of being punished by a chart they never saw, people can “work the system” and get the best company at he best rates through the Final Expense Guy.

CONCLUSION

Weigh charts are essential underwriting tools for the life insurance industry. You may feel they are unfair, but with the right company, you can find the best possible coverage.

If you want competent help and honest answers, speak to the Final Expense Guy.

He can share options for insurance coverage if you are committed to finding the best life insurance for your family.

FREQUENTLY ASKED QUESTIONS

How do insurance carriers determine limits of weight by height for rate classes? Insurance carriers reference height and weight charts when developing their maximum or minimum weight limits for each height when setting rate classes.

How height and weight impact life insurance premiums and rates? Your weight and height can be factors that will raise or lower your premiums since you may fall into different rate classes.

Do height and weight underwriting guidelines for life insurance differ for each company, age, health, and type of policy? Yes, each life insurance company has an underwriting chart, or not. They all differ based on age, health, and type of policy.

What happens if you exceed the life insurance build chart limits? If, according to the build chart guidelines, you are “over build”, you must either pay more for your life insurance through that company or apply and possibly go through a full medical evaluation. You could also consider final expense coverage, as there are some companies that don’t ask for your height and weight.

Which life insurance companies have more lenient weight rules and more forgiving classes for your build? Certain life insurance companies give a little more leniency on build charts. It largely depends on what state you live in and what plans are available in your state.

Do final expense policies have no height or weight requirements for seniors? Final expense policies typically have looser underwriting build charts, and some even have no build chart requirements. This is great for seniors!

Does guaranteed issue life insurance eliminate the build chart and health questions, and what does this mean for cost? Guaranteed issue policies don’t have a build chart. They ask no health questions, require you to have a 2-year wait before your policy starts, and it will be much more expensive.

How can you lower your insurance rate if you have been overweight, but have had a gradual loss in weight? It’s best to have a broker, like the final Expense Guy, help you find coverage based on your current health situation.

How does BMI affect rates when companies also consider labs and other health factors? The higher your BMI, generally the higher your life insurance cost, but the insurance companies will also consider your prescription medications, lab samples, and other health factors.

Show weight differences by insurance companies for the same height, 5’8″, and what it can mean for 200 pounds versus 190 pounds. – If you are 5’8″, company A may permit a weight of 200 pounds, while company B may put that limit at 190.