AARP Life Insurance Review – Is It Worth It?

Here’s the Bottom Line:

• AARP term life insurance ends coverage right when you need it most

• Rates increase over time and can become very expensive later on

• Coverage amounts are often too low to fully protect your family

• Guaranteed acceptance plans come with a costly 2-year waiting period

• You’re paying more for a brand name than the actual insurance value

AARP life insurance sounds simple, but it comes with trade-offs that most people don’t catch up front. Their term life insurance gets more expensive as you age and completely ends at age 80, leaving you exposed later in life. Their whole-life and guaranteed-acceptance options limit how much coverage you can get and often include a 2-year waiting period before full benefits pay out. That means your family could still be stuck with bills when it matters most. If you don’t look closely, you’ll likely overpay for less protection.

Complete my quote request form on this page to quickly see better options.

DOES AARP OFFER FIRST-DAY COVERAGE?

Only one AARP plan pays the full benefit right away, while the most promoted option delays real protection for 2 years.

Only the Permanent Life plan provides immediate benefits after approval.

The Guaranteed Acceptance application version, the one often promoted, is a guaranteed-acceptance policy with a MANDATORY two-year waiting period.

If death occurs during those first two years, your family receives only the premiums you paid plus a token amount of interest, typically around 7-10%. No full death benefit, no real protection.

True first-day coverage comes from simplified-issue whole-life insurance. These policies skip the medical exam but include a few basic health questions.

When approved, they pay the entire death benefit from day one, but these are rarely the best choice in the marketplace.

The marketing phrase “coverage starts immediately” only means you begin paying premiums right away, not that your family receives the full benefit. The restriction is often found in the fine print, where most people never look.

⚠️ Coverage Starts Immediately Mailer

Helen, 72, received an AARP mailer that described immediate coverage, which led her to enroll believing her family would receive full benefits right away.

The postcard arrived with bold lettering and a return envelope. Helen filled it out the same afternoon because she had just attended a neighbors funeral and didn’t want her kids dealing with paperwork or delays.

The hidden issue was that the Guaranteed Acceptance version she enrolled in carried a 2-year waiting period, and the phrase she relied on only meant premium billing started immediately.

I reviewed the certificate wording line by line and showed her where the waiting period blocked the death benefit for natural causes.

We replaced it with a simplified issue whole life plan that paid a $20,000 benefit immediately on approval to cover burial and final expenses.

CONS OF AARP BURIAL INSURANCE

AARP policies fall short because they cost more, limit coverage, and add restrictions that don’t help families.

First, the Level Benefit Term Life plan ends at age 80. If you live beyond that point, the coverage disappears, and every premium paid is gone. For people buying protection meant to last a lifetime, that’s a serious problem.

Second, the Guaranteed Acceptance plan requires a mandatory two-year waiting period. If death occurs during that time, the company refunds only premiums plus a small amount of interest, often around 7-10%. Your family does not receive the death benefit.

Third, the coverage limits are low for some people. Even their “Permanent Life” option caps at $100 000.

Finally, the pricing is inflated. Independent rate comparisons show AARP premiums running 25% to 60% higher than equivalent first-day coverage from top-tier carriers.

AARP insurance seems to be a brand-driven product sold at a markup to members who trust the name.

AARP BURIAL INSURANCE PRODUCTS

AARP sells 3 different policy types, and each one comes with tradeoffs most buyers don’t notice at first.

Here’s what you actually get when you look past the brochures:

Level Benefit Term Life – Coverage lasts until age 80. Premiums start low but increase every five years. That pattern makes it far more expensive over time than most people realize.

Once you reach 80, the policy expires. There is no refund or conversion into permanent coverage. Families who rely on this policy often find themselves uninsured exactly when they need it most.

Permanent Life Insurance – This option provides lifetime coverage with fixed premiums and a modest cash value. The maximum benefit is $100 000.

Because it asks a few health questions, it can pay from day one for those who qualify. However, the price per thousand of coverage is among the highest in the industry. You are paying for name recognition, not value.

Guaranteed Acceptance Life Insurance – This is a guaranteed-issue whole life insurance plan that sounds comforting but comes with a two-year waiting period.

Coverage tops out at $30,000. It is intended for applicants with major health problems who cannot qualify elsewhere. For everyone else, it is a poor financial choice.

WARNING!!! All three policies are group certificates owned under AARP’s master contract with New York Life. That means AARP controls key terms. You don’t own a stand-alone individual policy that you can move or customize.

HOW AARP LIFE INSURANCE REALLY WORKS BEHIND THE SCENES

AARP life insurance operates as group coverage controlled by AARP rather than an individual policy you own.

That means AARP, not you, controls your main policy document.

You receive a certificate of insurance that provides coverage under their group agreement. It’s not the same as owning a stand-alone individual policy that you can customize, move, or negotiate.

WARNING!!! AARP can change terms, benefits, or pricing structure under the group contract, while an individual policy stays fixed for life once issued.

New York Life makes it clear on its official site: each AARP plan is governed by the group policy issued to the Trustee of the AARP Life Insurance Trust. That’s public record. You can read it right on their website page.

So yes, it’s absolutely true. These are group certificates. You’re paying into a policy that AARP manages collectively, not one that belongs solely to you.

The structure is simple. New York Life provides the insurance. AARP lends its brand and member list. You pay for both. That is why AARP plans consistently cost more than direct-to-consumer options.

Group coverage also means limited flexibility. You cannot negotiate underwriting terms, reduce internal fees, or lock in custom riders. The pricing already includes the royalty paid to AARP.

AARP LEVEL BENEFIT TERM LIFE INSURANCE

This plan looks cheap early on, then gets expensive and disappears completely at age 80.

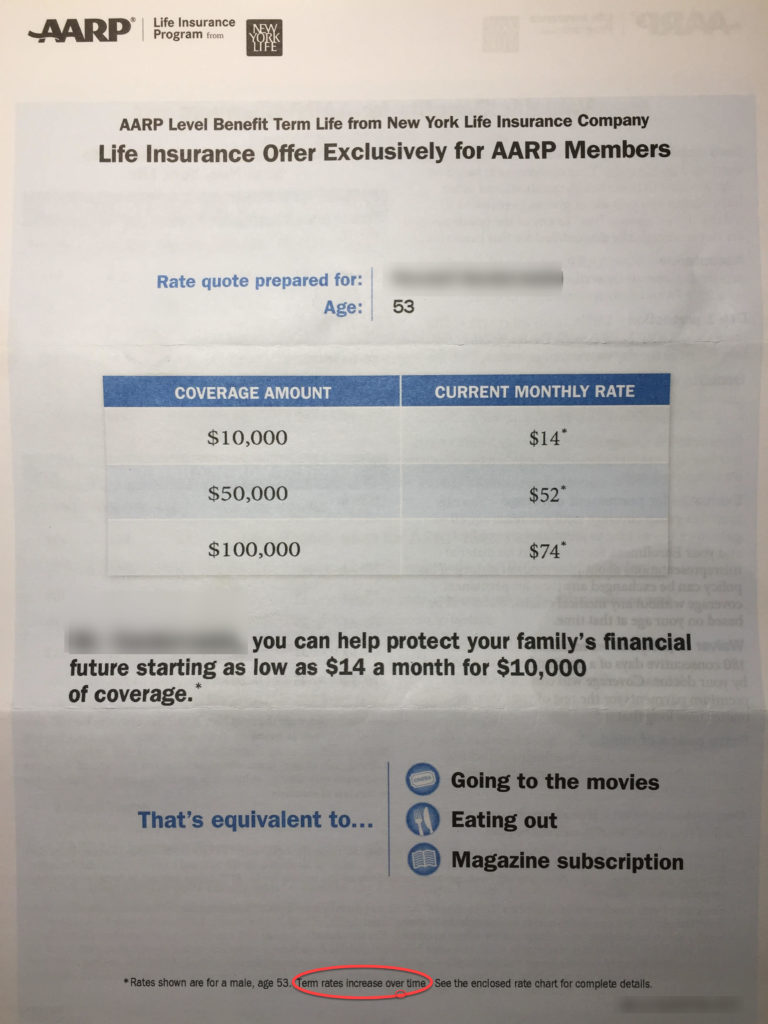

It’s available to members aged 50 to 74 and their spouses/partners aged 45 to 74, with coverage amounts up to $150,000. The price starts low but climbs every five years as you age.

The phrase “level benefit” confuses people. It only means the death benefit stays level, not the premium. The cost increases on a fixed schedule. By the time you reach your mid-seventies, many policyholders are paying double what they started with.

Even worse, the policy expires after age 80. You could pay into it for twenty or thirty years and lose every dollar when you outlive the term.

If you want lifetime coverage, this is the wrong product. The renewal increases are designed to encourage seniors to leave the policy once the cost becomes too high. That keeps New York Life’s risk low while maintaining high profits.

AARP PERMANENT LIFE INSURANCE REVIEW

This policy offers lifetime coverage with first-day benefits, but the price is far higher than similar plans elsewhere.

It’s a policy with level premiums and a small cash value. Issue ages range from 50 to 80, with coverage up to $100,000.

The application includes a few health questions. Those questions determine eligibility for first-day protection. The company claims acceptance for most applicants, but the pricing is steep.

For example, a healthy 65-year-old woman might pay over $130 per month for $25,000 in coverage through AARP Permanent Life. The same coverage through an independent whole-life carrier averages $96 per month.

The plan’s only real benefit is predictability. Premiums stay level and coverage never expires. The cash value grows slowly and rarely exceeds 10% of the death benefit. And, it’s still expensive!

AARP GUARANTEED ACCEPTANCE LIFE INSURANCE

This plan skips health questions but delays real insurance protection for a full 2 years.

It has a MANDATORY two-year waiting period. If you pass away during those first twenty-four months, your beneficiary receives only the premiums paid plus about 7-10% interest. Only accidental deaths pay the full benefit immediately.

This design protects the insurer, not the policyholder. It’s meant for people who are already in poor health or who would otherwise be declined.

AARP FINAL EXPENSE INSURANCE RIDERS

AARP riders add complexity and cost without giving most seniors meaningful extra value.

Each plan is issued through New York Life, and the most common add-ons are the Accelerated Benefit Rider and the Accidental Death Benefit Rider.

The Accelerated Benefit Rider lets you use part of your death benefit early if a doctor certifies you are terminally ill. The payout is usually up to half of your policy’s benefit, and you must be expected to live 24 months or less in most states, or 12 months or less in New York.

Whatever you take out now reduces what your family receives later. It’s not extra money. It’s just using your own benefit early.

The Accidental Death Rider pays an additional amount if your death meets the insurer’s definition of an accident. That may double the payout in some cases, but the fine print limits what counts as “accidental.” Death from illness, complications after surgery, or most workplace incidents are typically excluded after retirement.

Some marketing pieces mention chronic or critical-illness riders, but those are not standard and depend on the state where you live. They require extra underwriting and often cost more than they’re worth.

These riders are designed to make the policy appear flexible, yet most seniors never need to use them. The small extra premiums could buy a stronger first-day coverage plan that pays faster and costs less.

🔍 The Agent Who Mentioned an Accidental Rider

Frank, 68, spoke with a phone agent who highlighted an accidental death rider, which led him to believe his policy paid in full from day 1.

The conversation focused on peace of mind, and the rider was described as extra protection that kicked in right away. Frank assumed that meant the base policy worked the same way.

The missing detail was that accidental death riders don’t pay for medical or illness related deaths, and most deaths at his age wouldn’t qualify as accidental under the policy language.

I explained “accidental death” rider definition so he could see how limited the payout conditions really were.

I was able to help him qualifiy for a first-day coverage whole life plan with a $15,000 benefit that paid immediately for funeral and cremation costs.

COMMON MISLEADING AARP TERMS AND WHAT THEY REALLY MEAN

AARP marketing uses comforting language that often hides limits, delays, and higher costs.

“Guaranteed Acceptance” – This means approval is automatic, but the payout is not. A two-year waiting period always applies. During that time, only accidental deaths are eligible for full benefits.

“Coverage Starts Immediately” – This means your policy becomes active, and premiums are due. It does not mean the death benefit is payable right away. Many consumers mistakenly believe this is first-day coverage when, in fact, it is only administrative activation.

“Level Benefit” – This term refers to the amount paid to your beneficiary, not your monthly premium. The benefit remains level, but the cost increases over time for term policies.

“No Medical Exam Required” – This may seem convenient, but it also limits the insurer’s ability to accurately assess risk. That lack of data can significantly increase your price. You pay more for their uncertainty.

“Cash Value” – Whole-life plans do build cash value, but it accumulates slowly and is reduced by policy fees. It’s not an investment. It’s a partial refund of the extra premium you’ve paid.

Knowing these definitions separates honest coverage from clever marketing.

PROS OF AARP FINAL EXPENSE LIFE INSURANCE

AARP policies offer convenience and brand familiarity, not strong value or low pricing.

They’re backed by New York Life, one of the oldest insurers in the country with an A++ rating from A.M. Best. They don’t require a medical exam. The applications are short and can be completed by mail or phone. Coverage is available to people who have been turned down elsewhere.

Those are conveniences, not advantages. The lack of a medical exam means you’re automatically lumped into a higher-risk category. Insurers charge more when they know less about your health.

The small benefit amounts, typically $25,000 to $50,000, make these policies easy to approve but expensive per dollar of coverage.

For seniors with major medical issues who cannot qualify elsewhere, the Guaranteed Acceptance plan is at least a way to leave something behind; however, there are much better plans available through other companies.

CONSUMER COMPLAINTS AND PUBLIC FEEDBACK TO AARP LIFE INSURANCE

Public feedback shows frustration with pricing, waiting periods, and unclear enrollment disclosures.

Financial strength ratings demonstrate that claims are paid, and complaint ratios indicate how many buyers feel misled.

If a company has a high complaint ratio and relies on guaranteed-acceptance mailers, expect more fine print and higher prices. If the ratio is low and the plan offers first-day coverage with simple underwriting, you are likely getting better value.

Better: Verify the complaint index, then compare first-day coverage quotes before you sign anything.

HOW TO COMPARE FINAL-EXPENSE CARRIERS (NOT JUST AARP)

Smart comparison focuses on waiting periods, ownership, pricing, and complaint history instead of brand names.

Financial Strength – Check the insurer’s rating with A.M. Best, Moody’s, or Standard & Poor’s. Ratings show the company’s ability to pay claims. Look for an “A” or higher, but remember: high ratings do not guarantee low prices. They measure solvency, not honesty.

Complaint Ratios – Review each carrier’s NAIC Complaint Index. A score of 1.00 is average. Anything higher means more complaints than normal. The best final-expense companies often have ratios below 0.50.

Underwriting Method – Simplified-issue policies ask a few yes-or-no health questions. Guaranteed-issue plans skip them entirely and add a two-year waiting period. If you can qualify for a simplified issue, do it.

Price and Value – Always compare the monthly rate, not just the coverage amount. AARP’s $20,000 Guaranteed Acceptance plan for a 65-year-old woman could be as high as $110 per month. The same coverage through Mutual of Omaha could cost as little as $78, and Trinity Life averages $79 with first-day coverage.

Ownership Type – Group association policies, like AARP’s, are owned under a master contract. You do not control the terms. Individual policies give you ownership rights and protection under state law.

💡 High Rating Assumption

Mutual of Omaha coverage marketing implied financial safety through strong ratings, which led Carol, 67, to assume any plan offered would work for burial planning and move forward without comparing policy types.

Carol saw a television ad highlighting long company history and strong A.M. Best scores and called the number shown, believing high ratings automatically meant the best option for final expenses.

What she missed was that the agent steered her toward a guaranteed-issue option even though her health allowed simplified underwriting, quietly locking her into delayed benefits.

I reviewed her application history, confirmed her health answers qualified for simplified issue, and replaced the plan with an individually owned policy that paid a $20,000 benefit immediately for burial and final bills.

WHEN AARP MIGHT NOT BE THE BEST CHOICE AND WHAT TO ASK INSTEAD

Most seniors should ask direct questions that quickly reveal whether AARP makes financial sense.

Red flags to check with any agent:

If an agent avoids these questions, that is your answer. An independent simplified issue whole life policy is usually the smarter buy.

STATE VARIATIONS YOU SHOULD BE AWARE OF

State rules, costs, and advertising limits affect how AARP policies work and how much funerals really cost.

Some states restrict terms such as “state-regulated benefit” or “government-approved plan” because they can mislead consumers into thinking the product is sponsored by the government. AARP’s partners have faced compliance warnings in states such as Texas and Florida for using similar advertising language.

Funeral expenses and inflation rates differ, too. The National Funeral Directors Association (NFDA) reports that the average funeral cost in 2024 was $8,300 nationwide, but exceeded $9,500 in states such as Massachusetts and New York.

Understanding local rules helps you choose the right plan. An independent broker licensed in all states can compare policies side by side within your state’s limits.

FINAL VERDICT- IS AARP WORTH IT?

For most people, AARP life insurance delivers less coverage at a higher price than better first-day options.

AARP plans cost more, cover less, and include more restrictions than most independent first-day coverage options through brokers like the Final Expense Guy.

Their group ownership structure means you are not buying an individual policy. You are renting space under AARP’s master contract with New York Life. That design makes it easy for them to profit and difficult for you to compare apples-to-apples.

The two-year waiting period on the Guaranteed Acceptance coverage is the deal breaker for most families. AARP promotes it as protection, but it functions more like a savings plan that only becomes real insurance after two years. That delay can leave families with nothing when they need help the most.

The Permanent Life plan offers first-day coverage, but it can cost nearly twice as much as comparable whole-life policies sold directly through independent brokers. The Term Life option disappears after age 80, rendering it useless for burial or legacy planning.

For most seniors, the smarter move is a simplified-issue whole-life plan that pays from day one. Companies such as Trinity Life, Family Benefit Life, and Aetna consistently outperform AARP in price, transparency, and customer satisfaction.

AARP’s name recognition creates trust, but trust without value is a trap. The plan feels safe because it is familiar, yet the fine print quietly erodes that comfort.

💡 Assuming Permanent Meant Personal Ownership

Linda and Mark, both 70, chose AARP Permanent Life because the word permanent implied a policy they fully owned and controlled.

They enrolled after a short phone call and stored the paperwork in a drawer, assuming nothing could change once it was active.

The issue was that the coverage was issued as a group certificate under AARP’s master contract, not an individual policy with fixed personal ownership rights.

I explained how group certificates work and why terms are governed by the association rather than the insured.

I helped them switch to an individually owned whole life policy that paid a $25,000 benefit immediately to handle burial, medical balances, and family expenses.

FREQUENTLY ASKED QUESTIONS: AARP LIFE INSURANCE

How much is AARP life insurance a month?

AARP and New York Life do not publish universal monthly prices. Rates are product-specific and are only shown after you complete the online quote for your age, state, product, and eligibility. A single monthly figure is not publicly available. If you want predictable lifetime coverage without guessing, the Final Expense Guy can quote multiple top carriers side by side and show you written premiums before you decide.

How much does AARP charge for life insurance?

Costs vary by product and applicant, and there is no public master rate chart. The program lists coverage ranges and product rules, but you must run a quote to see actual premiums. If you want published, fixed whole life options that do not expire and do not require a medical exam, the Final Expense Guy can provide verbal quotes from multiple A-rated carriers so you can compare features and disclosures in black and white.

Is life insurance through AARP worth it?

That depends on your need and the product details AARP publicly discloses. Their products are rarely competitive with those of other insurance companies. Their term life offers coverage amounts up to $150,000 and can last until age eighty, with rates that increase over time. Permanent Life is whole life coverage up to $100,000 with rates that do not increase. Guaranteed Acceptance is whole life up to $30,000, with no health questions and limited benefits during the first two years. None of those pages publishes universal premium tables. To decide if it is worth it, compare these features against first-day coverage whole life from independent carriers. The Final Expense Guy can put those options next to AARP on the same page and keep only what fits your goals.

Does AARP offer life insurance for seniors over 75?

Yes, for specific products. Permanent Life is available to AARP members ages fifty to eighty and spouses or partners ages forty-five to eighty. Guaranteed Acceptance indicates availability for members up to age eighty-five, with state variations noted on AARP’s page. Term Life accepts members up to age seventy-four and can last until age eighty. If you are over seventy-five and want lifetime coverage that does not expire, the Final Expense Guy can quote multiple simplified issue whole life options that do not cut off at age eighty.

At what age does AARP life insurance end?

Term Life can last until age eighty if premiums are paid. Permanent Life and Guaranteed Acceptance are designed as whole life coverage and do not list a fixed end age on the public pages. If you want coverage that never ends and premiums that never rise, the Final Expense Guy can show whole life options from multiple insurers with clear, lifetime wording in the policy.

Is AARP good life insurance for seniors?

AARP’s public pages confirm three things seniors should weigh before buying. Term Life can end at age eighty and has rate increases over time. Permanent Life offers guaranteed rates that never increase and coverage up to $100,000. Guaranteed Acceptance has a two-year limited benefit period. Whether that is good for you depends on your health and budget, and there are no public rate tables. The Final Expense Guy can quote first-day coverage, whole life from several carriers, so you can compare guaranteed lifetime protection without a waiting period.

How long does it take for AARP life insurance to pay out?

New York Life’s AARP pages describe how to file a claim but do not publish a guaranteed payout timeline. They do state that Guaranteed Acceptance has limited benefits during the first two years, which affects what is payable during that period. If you want a fast, direct benefit payment to your beneficiary without a limited benefit period, the Final Expense Guy can show whole life plans that pay the full amount from day one upon approval.

What are the major problem issues of AARP?

Policies are underwritten by New York Life and issued as group coverage held by the AARP Life Insurance Trust. AARP discloses that New York Life pays royalty fees to AARP for the use of its intellectual property, and that the complete terms are in the group policy issued to the Trustee. Product pages also disclose that Term Life rates increase over time and can last to age eighty, and that Guaranteed Acceptance has limited benefits in the first two years. If you prefer an individual policy you own directly, with lifetime guarantees and no two-year limitation, the Final Expense Guy can present independent whole life options that meet those criteria.

What life insurance company does AARP recommend?

All AARP-branded life insurance in this program is underwritten by New York Life Insurance Company, as disclosed on the AARP and New York Life pages. AARP is not the insurer, and it does not service the policies. If you want alternatives beyond a single underwriting company, the Final Expense Guy can compare multiple A-rated insurers so you see your choices on one call.

3 Comments

Gracie Howard for Vivian Howard

Vivian is my Mother-In-Law. She’s 90 years old. No life insurance. We are interested in burial insurance only. Please contact me via email with rates etc as my son (POA) will be the principle. We look forward to receiving info today as we need to get this in place. Thank you.

Final Expense Guy

Gracie – There are no insurance companies that offer insurance for someone who is 90 years old.

Dave

Need burial insurance