Colonial Penn $9.95 Life Insurance Review – Truth Revealed!

Here’s the Bottom Line:

• The $9.95 price hides how little coverage you actually get

• Coverage shrinks as you age, even though the price stays the same

• Most policies have a 2-year waiting period before full payout

• You often pay more for less coverage than other companies

• “Units” make it hard to understand real cost and value

• Complaint levels are higher than most competing insurers

Colonial Penn burial insurance is a guaranteed-acceptance whole-life policy designed primarily for seniors who can’t qualify elsewhere. The appeal is simple: no health questions and easy approval. The problem is cost and value. Their “unit” pricing means $9.95 doesn’t buy much coverage, especially as you get older, and most policies include a 2-year waiting period before full benefits pay out. Compared to other burial insurance options, coverage is usually lower, and pricing is higher, which is why many people end up overpaying for less protection.

Complete my quote request form on this page to get real coverage without overpaying or guessing.

WHAT IS COLONIAL PENN’S $9.95 LIFE INSURANCE PLAN?

Colonial Penn sells guaranteed acceptance whole life insurance using a unit system that gives very small coverage for each $9.95 payment.

The company has been around for decades and markets heavily to seniors through television commercials featuring familiar faces and comforting music.

The ad sounds simple because they offer life insurance for only $9.95 a month, guaranteed acceptance, and no health questions. But what they don’t emphasize is that $9.95 only buys one “unit” of coverage. It’s not a full policy. It’s only a partial policy for about 99.9% of seniors.

Each “unit” equals a small amount of death benefit, usually between $400 and $1,500, depending on your age and gender.

The older you are, the smaller your benefit per unit. You can buy multiple units, but each additional unit costs another $9.95!

For someone who needs $10,000 in protection, the real price could be $60 to $120 per month, not $9.95. Even over $200 a month is not uncommon.

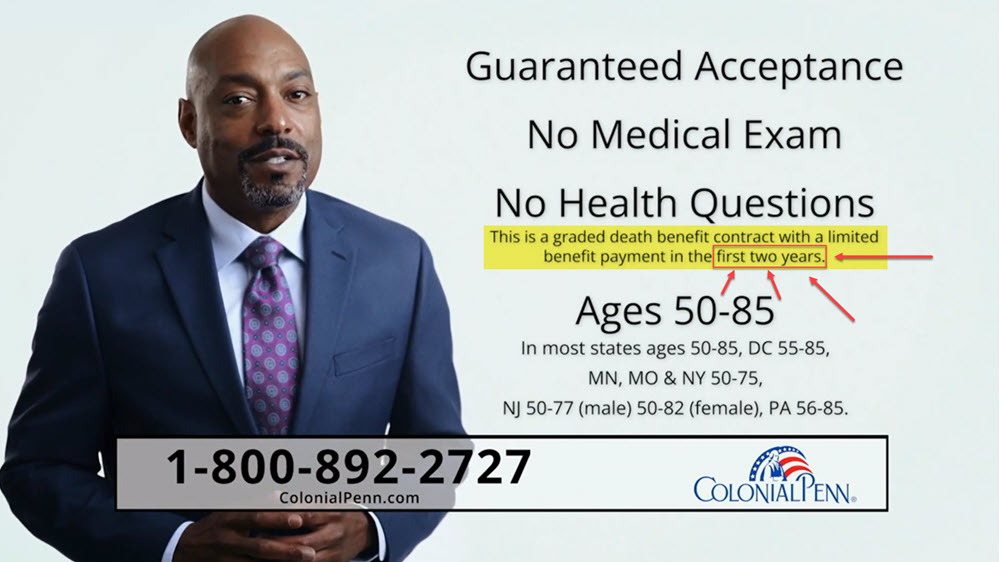

It’s also important to know that this plan is guaranteed issue, which means the company doesn’t ask health questions. Everyone gets approved if they can afford the outlandish prices Colonial Penn charges.

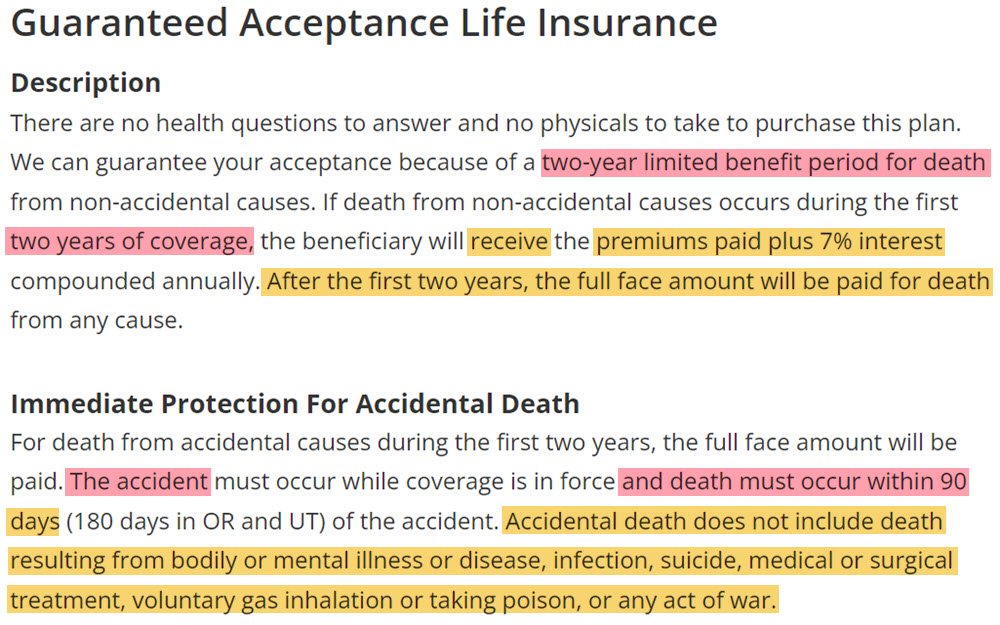

Because Colonial Penn accepts everyone, it forces everyone into a two-year waiting period.

If you pass away from natural causes during the first two years, your family doesn’t get the full benefit. They only refund what you’ve paid so far, plus a small amount of interest.

This structure protects the company, not you as a customer. It’s the tradeoff you make when you buy guaranteed acceptance life insurance instead of qualifying for massively better first-day coverage.

I’ve reviewed hundreds of these policies for families who thought they were protected. They weren’t.

HOW MUCH COVERAGE DO YOU REALLY GET FOR $9.95?

One $9.95 unit usually buys only a few hundred dollars of coverage, so real protection costs many times more than the ads suggest.

According to Colonial Penn’s official rate chart, here’s exactly what one $9.95 unit buys:

| Age | Male Coverage |

Female Coverage |

|---|---|---|

| 50 | $1,669 | $2,000 |

| 51 | $1,620 | $1,942 |

| 52 | $1,565 | $1,890 |

| 53 | $1,515 | $1,845 |

| 54 | $1,460 | $1,802 |

| 55 | $1,420 | $1,761 |

| 56 | $1,370 | $1,719 |

| 57 | $1,313 | $1,669 |

| 58 | $1,258 | $1,620 |

| 59 | $1,200 | $1,565 |

| 60 | $1,167 | $1,515 |

| 61 | $1,112 | $1,460 |

| 62 | $1,057 | $1,420 |

| 63 | $1,000 | $1,370 |

| 64 | $949 | $1,313 |

| 65 | $896 | $1,258 |

| 66 | $846 | $1,200 |

| 67 | $802 | $1,167 |

| 68 | $762 | $1,112 |

| 69 | $724 | $1,057 |

| 70 | $689 | $1,000 |

| 71 | $657 | $949 |

| 72 | $627 | $896 |

| 73 | $608 | $845 |

| 74 | $578 | $802 |

| 75 | $550 | $762 |

| 76 | $521 | $724 |

| 77 | $493 | $689 |

| 78 | $468 | $657 |

| 79 | $448 | $627 |

| 80 | $426 | $608 |

That means a 75-year-old man paying Colonial Penn $9.95 a month only has about $550 in life insurance. To reach $10,000 in coverage, he’d need 18 units, which would cost $179.10 per month.

Compare that to most first-day-coverage final expense plans, where a healthy 75-year-old woman might pay $71 per month for a $10,000 policy that pays immediately, not after two years.

The difference isn’t small, it’s massive. You’re paying more, waiting longer, and getting less coverage.

Colonial Penn’s $9.95 plan was designed for people with serious health conditions who can’t qualify anywhere else. But most applicants can.

⚠️ One $9.95 Unit Meant One Big Misunderstanding

Colonial Penn’s $9.95 unit-based life insurance implied meaningful protection, which led Frank to believe he had full funeral coverage in place.

Frank was 74 and called after seeing the $9.95 TV commercial during the evening news. He said the ad made it sound like one small payment locked everything in, and he’d been paying on the policy for over a year without ever looking at the paperwork.

The hidden issue was the unit structure. He thought $9.95 bought a policy. It bought a fraction of one. His single unit only covered a small portion of final costs, and nothing in the ad explained how many units were actually needed.

I reviewed his policy, walked through the unit chart, and showed what his coverage really amounted to. We replaced it with a $10,000 whole life policy that pays immediately and will cover burial, funeral services, and related final bills.

DOES COLONIAL PENN HAVE A WAITING PERIOD?

Colonial Penn delays full payouts for natural death during the first 2 years, refunding premiums instead of paying the benefit.

That means if you pass away from natural causes within the first 24 months, your loved ones will not receive the full death benefit. Instead, Colonial Penn refunds the premiums you’ve paid, plus a small amount of interest at 7% total.

That’s the tradeoff when a company promises “guaranteed acceptance.” They can’t ask about your health, so they protect their bottom line by delaying when your coverage actually starts.

During those two years, only accidental deaths, like a car accident or a fall, would pay the full benefit. Any other cause, including a heart attack, cancer, or stroke, would not.

This is the single most misunderstood part of the Colonial Penn $9.95 offer. The ads never clearly say, “There’s a two-year waiting period before your coverage pays out.” They focus on comforting words like “peace of mind” and “guaranteed acceptance,” which sound safe but hide a terribly 2-year wait plan.

Guaranteed-issue life insurance like Colonial Penn’s should never be an option that you would consider.

- You probably qualify for 1st-day coverage through another company.

- If guaranteed issue is your only choice, there are other companies with massively lower pricing and between 10-30% refund of premium interest rates.

🔍 Guaranteed Acceptance, But Delayed Coverage

A guaranteed acceptance policy with a built-in waiting period caused Linda to believe her family would receive full benefits right away.

Linda was 69 and signed up after receiving a postcard in the mail that promised acceptance without health questions. She assumed that meant her children were protected the moment she was approved.

The missing detail was the 2-year waiting period for natural death. The policy refunded premiums during that window instead of paying the benefit, which defeated the reason she bought coverage in the first place.

I reviewed her health history and explained why the waiting period applied. We moved her into a $15,000 first-day coverage whole life policy designed to pay immediately for cremation, memorial services, and remaining medical expenses.

COLONIAL PENN BACKGROUND & FINANCIAL RATINGS

Colonial Penn is financially stable and long established, but its ratings don’t justify the high cost and weak value of the $9.95 plan.

It’s owned by CNO Financial Group, the same parent company that owns Bankers Life and Washington National.

Financially, Colonial Penn is stable enough to meet its obligations. According to A.M. Best, it holds an A (Excellent) financial strength rating, which is average.

While that’s not a red flag, it’s also not the strongest rating among major insurers. For comparison, companies like Mutual of Omaha and Aetna typically carry A- or A+ ratings.

The Better Business Bureau (BBB) gives Colonial Penn an A+ rating, but that score reflects how they respond to complaints, not how satisfied customers are.

In fact, there are hundreds of complaints filed with the BBB and the National Association of Insurance Commissioners (NAIC), many about misleading marketing, poor communication, or confusion about coverage amounts.

Colonial Penn has been in business for more than 50 years, but its marketing hasn’t evolved with transparency…many seniors would say this is intentional.

COLONIAL PENN COMPLAINTS AND CONSUMER REVIEWS

Many customers report confusion, disappointment, and frustration after learning how little coverage they actually received.

On the Better Business Bureau (BBB) site, you’ll find thousands of reviews and complaints mentioning the same pattern: seniors believe they’re buying a full life insurance policy for $9.95, only to discover it buys one “unit” of coverage worth a few hundred dollars.

Others report that their claims were delayed or denied because the death occurred during the two-year waiting period.

Many families also describe frustrating customer service experiences. Calls can take hours, paperwork often requires mailing physical forms, and cancellation or policy adjustments can be slow.

On Trustpilot, Colonial Penn’s rating sits below most major insurers, with recurring themes of misleading advertising, poor communication, and unclear benefit explanations.

The National Association of Insurance Commissioners (NAIC) also shows Colonial Penn with a complaint index higher than the industry average. That means the company receives more complaints relative to its size than most competitors.

WHO IS THE COLONIAL PENN $9.95 PLAN GOOD FOR?

This plan only fits people who can’t qualify anywhere else and are willing to accept high costs and delayed benefits.

Even at that, you’re better off going with other companies that the Final Expense Guy is qualified to help you with.

Funeral Cost Percentage Breakdown

If you’ve been declined multiple times due to advanced illness, such as terminal cancer, late-stage heart disease, or oxygen dependency, then Colonial Penn’s guaranteed-issue plan could work…if it weren’t so overpriced.

For everyone else, it’s usually a bad deal. Most people over age 50 can qualify for simplified-issue whole life insurance with first-day coverage, no medical exam, and just a few basic health questions. Those plans cost less per dollar of coverage, have higher benefits, and start paying immediately.

The difference can be dramatic. For example, a 65-year-old woman with mild health conditions could pay $41 per month for a $10,000 first-day coverage policy from a top-rated carrier like Trinity Life or Family Benefit Life. The same amount of coverage through Colonial Penn would cost around $79.60 – and still include a two-year waiting period.

Colonial Penn markets heavily to seniors on fixed incomes, but it’s those same families who end up paying more and receiving less.

💡 Accidental Coverage Wasn’t the Plan

A policy structured to favor accidental death payouts led Robert to think any cause of death would trigger the full benefit.

Robert was 76 and enrolled after speaking with a phone agent who emphasized peace of mind without explaining how deaths were treated differently. He assumed the coverage worked the same regardless of cause.

The misunderstanding was that only accidental death paid the full amount during the first 24 months. Natural causes fell under the waiting period, which wasn’t explained clearly during the call.

I broke down the policy language and clarified how claims were handled. We replaced it with a $20,000 immediate-pay whole life policy intended to cover funeral costs, burial expenses, and outstanding household obligations.

BETTER ALTERNATIVES TO COLONIAL PENN

Most seniors can qualify for first-day coverage whole life policies that cost less and pay out immediately.

The key difference is choosing simplified-issue whole life insurance instead of guaranteed-issue coverage.

Simplified issue means you’ll have to answer a few short health questions. There is no medical exam, and decisions are made instantly. These plans pay from the very first day, not two years later. They are backed by financially strong, A-rated carriers that specialize in final expense coverage for seniors. And you’re rewarded with massively lower pricing.

Companies such as Trinity Life, Family Benefit Life, Aetna, and other companies consistently offer better value, stronger benefits, and faster payouts. These are the policies I recommend to my own clients.

Here’s a clear comparison of what real alternatives look like:

| $10,000 Coverage & Company | Female 50 y/o |

Female 60 y/o |

Female 70 y/o |

Male 50 y/o |

Male 60 y/o |

Male 70 y/o |

|---|---|---|---|---|---|---|

| FEXGUY #1 Carrier | $21 | $32 | $52 | $27 | $41 | $69 |

| AETNA – Accendo CVS Health | $27 | $40 | $58 | $31 | $51 | $73 |

| American Amicable | $26 | $38 | $60 | $31 | $47 | $78 |

| CICA Life | $31 | $49 | $83 | $33 | $55 | $102 |

| Gerber Life | $34 | $51 | $75 | $44 | $63 | $99 |

When you look at it this way, the difference is obvious.

First-day coverage plans offer stronger protection at nearly half the cost. And the money your family receives is guaranteed to pay out immediately, without fine print or delays.

HOW TO COMPARE FINAL EXPENSE POLICIES PROPERLY

The smartest comparison focuses on when coverage pays, how much it really costs, and how strong the insurer is.

To compare correctly, focus on four key points:

- When the coverage starts: If the policy includes words like “graded,” “modified,” or “return of premium,” it means there is a waiting period. Always ask if your coverage pays immediately.

- The stability of your premium: A proper whole life policy never increases in cost. If your quote says the price can go up, it is the wrong product.

- The total benefit amount: Always look at the payout your family will actually receive. A cheap policy with a small benefit is not real protection.

- The strength of the company: Check the A.M. Best rating before buying. Stick with insurers rated A or better.

| Feature | Colonial Penn | FEXGUY First-Day Coverage |

|---|---|---|

| Coverage Start | After 2-Year Waiting Period | Starts Immediately |

| Medical Questions | No (Guaranteed Acceptance) | Simple Health Questions for Better Rates |

| Monthly Cost for $10,000 (Age 65 Female) | $79 | $41 |

| Payout for Death in First 2 Years | Refund of Premiums + Small Interest | Full Death Benefit Paid |

| Transparency | Confusing “Unit” System | Clear Fixed-Benefit Coverage |

| Who It Helps | People Uninsurable Anywhere Else | Most Seniors in Decent Health |

| Customer Reviews | High Complaint Ratios (BBB & NAIC) | Top-Rated Carriers with Proven Claims History |

Working with an independent broker means you see multiple carriers side by side. That’s how you know you’re getting both the best rate and the right type of coverage.

FINAL VERDICT – IS COLONIAL PENN $9.95 A SCAM?

Colonial Penn isn’t illegal, but the $9.95 marketing hides poor value, delayed benefits, and overpriced coverage.

The Colonial Penn $9.95 offer hooks seniors with emotional messaging, then quietly delivers minimal coverage with a two-year waiting period.

The company relies on misleading television marketing, and the numbers simply don’t justify the overpriced rates. Paying $150-$200 a month for $10,000 of coverage that takes two years to activate is not a good deal.

For most people, there are far better options from the Final Expense Guy. Simplified-issue whole life policies from financially strong companies provide immediate benefits, lower premiums, and guaranteed lifetime coverage.

FREQUENTLY ASKED QUESTIONS: COLONIAL PENN $9.95 LIFE INSURANCE REVIEW

Is Colonial Penn life insurance legitimate?

Colonial Penn sells real-life insurance policies that are generally unsuitable for most people.

Colonial Penn is a legitimate insurance company owned by CNO Financial Group. The issue is not legitimacy; it is value. Their guaranteed-acceptance plan is legally sound but financially weak compared to what most people can qualify for.

What does “unit” mean in the Colonial Penn $9.95 plan?

A unit works like a chunk of coverage.

One unit usually equals $400 to $1,500 in benefit. The older you are, the less coverage you get per unit, and it is one of the most expensive ways to buy life insurance coverage.

Does Colonial Penn have a waiting period?

Colonial Penn’s guaranteed-acceptance policies come with a mandatory 2-year waiting period.

Every guaranteed-acceptance policy from Colonial Penn includes a two-year waiting period for natural causes. During that time, your family only receives the premiums you paid plus a small interest amount.

Can I get first-day coverage instead?

Many applicants qualify for day-1 coverage with simplified-issue whole life from the Final Expense Guy.

If you can answer a few basic health questions and are not in critical condition, you likely qualify for simplified-issue whole life insurance that starts immediately.

How much coverage will $9.95 buy at age 65 or 75?

The $9.95 price buys very little coverage at older ages.

At age 75, it drops closer to $560 for men and $680 for women. To reach a typical $10,000 benefit, the monthly cost is often well over $100.

What happens if I die within two years?

A death within the first 2 years triggers a refund rather than a payout.

The only exception is if the death was accidental.

Does Colonial Penn offer coverage for veterans?

Colonial Penn operates as a private insurance company.

Veterans are often better served through companies used by the Final Expense Guy. There is no need to settle for a 2-year waiting period and higher prices when you can qualify for much better rates just by shopping around.

Is Colonial Penn good for burial insurance?

Colonial Penn’s 2-year delay makes it a poor fit for burial costs.

Colonial Penn’s two-year delay defeats that purpose, leaving most people unprotected and overcharged for the rest of their lives.

Can I cancel and get a refund?

You can end your Colonial Penn policy whenever you want.

You will not get a refund of premiums unless it’s in the first 30 days.

What are the best life insurance alternatives to Colonial Penn?

Other whole life policies can cost less and start on day 1.

Simplified-issue whole life policies from companies like Family Benefit Life, Trinity, and Prosperity Life typically offer better rates, first-day benefits, and stronger financial ratings.