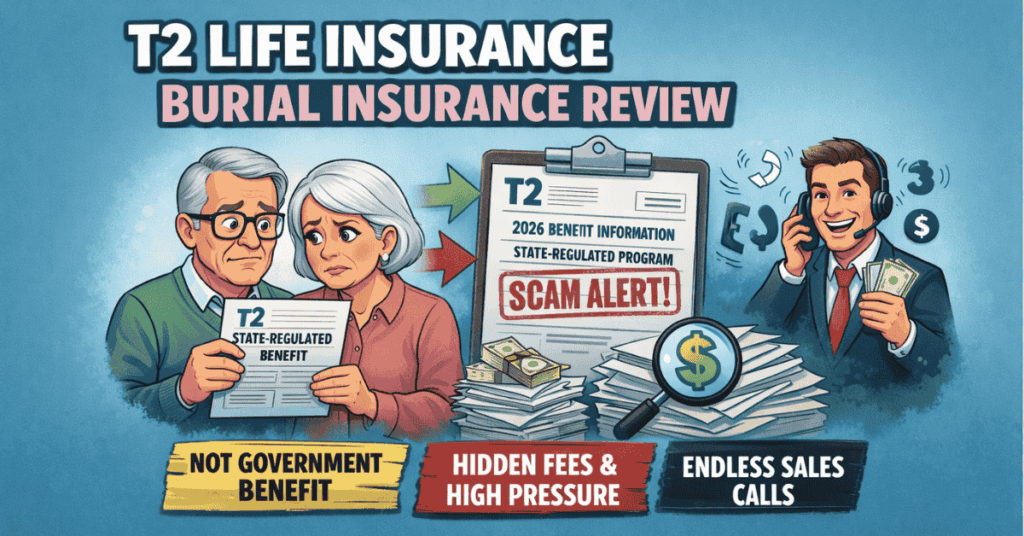

Is The T2 Form A SCAM?

last updated on April 14, 2026

last updated on April 14, 2026Here’s the Bottom Line:

• The T2 form is not a real government or official document

• It’s a marketing mailer designed to collect your personal information

• Filling it out leads to nonstop calls, texts, and sales pressure

• “Free benefits” claims are misleading and not real insurance offers

• You’ll likely be sold overpriced or poor-fitting life insurance plans

• Most people think it’s official, which is exactly the trap

The T2 form is a life insurance marketing mailer that’s made to look like a government notice, but it isn’t. It’s sent by lead generation companies to collect your name, phone number, and personal details so they can sell that information to agents. Once you send it back, you’ll usually get bombarded with calls and offers for burial insurance or whole life insurance, often at higher prices. There’s no such thing as “free” coverage tied to it, and it’s not connected to any state or federal program. That’s where people get misled and overpay.

Complete my quote request form on this page to get real options without scams or confusion.

IS THE T2 FORM AFFILIATED WITH ANY GOVERNMENT AGENCY?

The T2 Form has no link to Social Security, Veterans Affairs, Medicare, or any government office despite language that suggests otherwise.

The use of terms like “state-regulated,” “government benefit,” or “official request” is not a government designation, and many seniors call this a scam.

Under NAIC Model Regulation 570, any advertisement that suggests government sponsorship or approval without proof is considered misleading and non-compliant.

The Federal Trade Commission (FTC) and the National Association of Insurance Commissioners (NAIC) both monitor deceptive marketing practices in the insurance industry.

Several state regulators, such as the Texas Department of Insurance and the Florida Office of Insurance Regulation, have warned consumers to be cautious of any mailers or phone calls claiming to be tied to “new state burial benefits.”

A real government agency would never require you to fill out a postcard to receive burial coverage.

The only true government death benefit available to most Americans is the $255 lump-sum payment from the Social Security Administration after a qualifying worker’s death (if you even qualify). Everything else must come from a private life insurance policy.

WHAT INFORMATION DOES THE T2 FORM COLLECT?

The T2 Form gathers personal and sometimes health details that marketers use to identify, track, and resell you as a lead.

These forms appear harmless, but they give marketers everything needed to identify and target you for sales calls.

Once you submit a form, the form usually goes to a lead aggregator that stores the data in a database shared among multiple agents.

Your information can then be resold or “pinged” in a live bidding system where the highest bidder gains temporary access to call you. This is how telemarketers, call centers, and independent agents end up contacting the same person multiple times in a single week.

Because the data includes personal and health information, there are also privacy risks.

Some of these companies operate outside U.S. jurisdiction, which makes it difficult for regulators to enforce data protection under HIPAA, CAN-SPAM, and TCPA laws. Consumers who fill out these forms often experience an increase in unsolicited calls, texts, or emails within hours to days.

RED FLAGS THAT THE T2 FORM MAY BE A SCAM

The mailer uses misleading language, fake authority signals, and missing sender details that commonly show deceptive intent.

A second red flag is the language. Phrases such as “benefits available to all residents” or “new government-regulated program” imply a government connection that does not exist.

Some forms include small print disclaimers stating “not affiliated with any government agency,” but these disclaimers are often hidden or placed in a low-contrast section.

Another warning sign is the lack of clear sender identification. Legitimate insurance mailers must include a licensed agency name, address, and phone number.

Many T2 Forms list only a “Processing Center” or “Senior Benefits Office” with no license number. That omission violates NAIC Model Regulation 570 and several state-level marketing disclosure laws.

Consumers who complete these forms may receive hundreds of phone calls from different agents, which is another sign of a shared lead pool.

Complaints to the Better Business Bureau and state Departments of Insurance frequently describe repeated solicitations and high-pressure tactics following a form submission.

⚠️ The “Everyone Qualifies” Phone Call

A shared T2 lead triggered a phone call claiming universal approval, caused a widowed couple to skip questions, and led them to believe benefits would be immediate.

Marsha and Bill, both in their late 60s, got a call after returning a form that promised coverage “for all residents regardless of health.” The agent rushed through the conversation and focused on getting verbal confirmation instead of explaining how the policy worked.

The missing piece was the waiting period. The policy relied on a graded benefit clause that delayed full payout for natural causes, something the agent never explained clearly. They believed the phrase “everyone qualifies” meant the benefit would pay in full right away.

I stepped in, pulled the policy details, and showed them where the delay applied. We walked through underwriting honestly instead of avoiding it, which changed the options available.

They qualified for $20,000 of immediate whole life coverage designed to cover burial expenses and remaining household bills, with the full benefit payable from the first day.

WHAT IS THE T2 FORM?

The T2 Form operates as a direct mail solicitation designed to look like a government notice while serving only marketing purposes.

These forms typically include a few basic fields such as age, gender, health status, and phone number, as well as a prepaid return envelope.

Consumers often mistake them for something related to “state-regulated final expense benefits” or “burial assistance programs.”

In reality, no such government program exists. Each U.S. state regulates insurance companies individually, but there’s no state-run burial or funeral insurance plan.

The T2 Form typically references terms like:

- State Regulated Final Expense Program

- New Benefit Update 2025

- Senior Burial Coverage Information

- Government Benefit Verification Form

Each of these phrases is crafted to sound official, but the form itself has no connection to any government agency.

Instead, it’s used by private marketing vendors to capture your personal information to sell as “leads” to licensed agents or call centers.

Many mailers also include an “official” looking seal or shaded boxes resembling tax or SSA documents. This design tactic is prohibited under NAIC Model Regulation 570, which forbids any advertising implying government affiliation.

💡 The Official-Looking Postcard

The T2 Form mailer used government-style language, implied a state benefit, and led a retired school custodian to believe he needed to respond to keep burial coverage active.

Frank, age 71, pulled a postcard from his mailbox that said “Important Benefit Information” in bold print and referenced a “state-regulated final expense program.” He filled it out at the kitchen table that night, thinking it had something to do with Social Security because the layout looked familiar and the return envelope was prepaid.

The issue showed up once the calls started. The form never named an agency, carrier, or license number, and it never said the coverage would come from a private company. Frank assumed any policy tied to the state meant automatic approval and full benefits right away, which wasn’t what the form actually did.

I reviewed the mailer line by line and explained that “state-regulated” only meant the policy would be sold in the state, not provided by it. We scrapped the lead entirely and applied directly with a carrier that underwrote his health properly.

He ended up with $15,000 of whole life coverage that starts immediately and is intended to handle funeral costs and final medical bills, paying the full amount from day 1.

WHO SENDS THE T2 FORM?

Third party lead generation companies send the T2 Form to collect and resell consumer data for profit.

Many of these companies operate as “lead aggregators,” and they’re not licensed to sell insurance.

Their business model depends entirely on collecting consumer data and reselling it through “ping-post” systems, where multiple agencies bid for your lead in real time.

Some use shell DBAs (Doing Business As) that change frequently, making it difficult for regulators to track them. Others omit addresses or use vague return addresses like “Processing Center” or “State Benefits Department.”

In 2024, several state Departments of Insurance offices, including North Carolina, Florida, and Texas, issued consumer alerts about deceptive insurance mailers that used government-style language without proper disclosure.

These warnings specifically cited violations of Section 45 of the FTC Act, which prohibits unfair or deceptive advertising practices.

In short, the T2 Form isn’t illegal by itself, but how it’s used often crosses compliance lines. When used to mislead consumers or collect data without disclosure, it becomes part of a larger consumer deception pattern.

HOW T2 FORM LEADS ARE SOLD TO INSURANCE AGENTS

Submitted T2 Form data enters a bidding system where multiple agents can buy the right to contact the same person.

Lead aggregators upload the data to platforms where multiple agencies and individual agents can bid for access. This system is known as “ping-post lead routing”. The first agent to purchase the lead gains temporary calling rights, often within seconds of the form being received.

Because these leads are not exclusive, the consumer’s data can be sold multiple times to different buyers.

That is why a single T2 submission may result in several agents calling or texting in a short period. The lead seller profits each time the data is resold, regardless of whether a policy is ever issued.

Agents who purchase these leads often do not know the source. Many are unaware that the mailer implied government affiliation, which places them at risk for compliance violations if consumers complain.

Regulators have held agencies responsible for failing to verify the legality of their marketing sources.

The NAIC Unfair Trade Practices Act and several state-specific laws make it clear that agents are accountable for the actions of their marketing partners. This means even if the lead vendor creates the deceptive form, the licensed agent can still face penalties for using it.

WHY SOME LICENSED AGENTS STILL USE T2 LEADS

Some agents rely on T2 leads because they are cheap or because the deceptive source is hidden from them.

A typical shared T2 lead can cost between three and ten dollars, while an exclusive, verified lead may cost more than forty. For agents struggling to meet sales quotas, low-cost leads appear attractive.

Some agencies also justify the use of T2 leads by claiming the mailers are only “inquiries,” not advertisements. This interpretation attempts to avoid disclosure requirements under NAIC Model Regulation 570.

The problem is that regulators have repeatedly stated that any form implying a government benefit is subject to advertising and disclosure laws, regardless of how it is labeled.

Other agents are simply unaware of the form’s origin. Lead vendors frequently change company names and mailing templates, making it difficult to identify the real sender.

As a result, even well-meaning agents may contact consumers who filled out a deceptive form without realizing how that data was obtained.

Using these leads can cause consumers who feel tricked by a fake government mailer rarely trust the agent who calls them afterward, even if that agent is fully licensed.

🔍 The Agent Who Didn’t Know the Source

A ping-post lead from a T2 Form routed multiple agents to the same household and caused confusion about who actually collected the information.

Ray, a 63-year-old mechanic, answered 4 calls in 2 days after sending back a single postcard. Each caller claimed to be “following up” on his request, yet none could explain where the form came from or why others were calling him too.

The misunderstanding was that Ray thought he had contacted one office. In truth, his data had been resold through a live bidding system, and the agents calling him didn’t control the mailer or its wording.

I verified the source, explained how shared leads work, and stopped the cycle by moving the conversation away from the form entirely. We focused on carrier rules and his actual health profile instead of the lead.

Ray secured $25,000 in first-day whole life coverage meant to handle funeral and cremation costs plus final debts, with the policy paying the full benefit immediately upon death.

LEGAL AND COMPLIANCE ANALYSIS

Using T2 Forms can violate federal and state advertising laws when they imply government affiliation without proper disclosure.

The Federal Trade Commission (FTC) classifies deceptive mail practices as violations of Section 45 of the FTC Act, which prohibits unfair or misleading advertising.

The NAIC Model Regulation 570 and 572 outline similar standards for insurance marketing, requiring full disclosure of licensing information and prohibiting any implication of government affiliation.

When companies use the T2 Form to collect leads without proper disclosure, they risk penalties from both state and federal regulators. Violations may lead to fines, cease-and-desist orders, or license suspension if tied to a licensed agency.

The Telephone Consumer Protection Act (TCPA) also applies when the information collected is used for unsolicited calls or texts without prior written consent.

State Departments of Insurance in California, Texas, and North Carolina have each released consumer alerts about misleading “state benefit” mailers. These alerts emphasize that legitimate insurance programs require licensed agents to identify themselves and the carrier before discussing coverage.

Consumers who suspect deception can report violations directly to the FTC Complaint Assistant, state DOI, or NAIC Consumer Information Source. These agencies maintain active databases for tracking patterns of deceptive marketing.

HOW TO VERIFY IF A T2 FORM CONTACT IS LEGITIMATE

A legitimate agent can be confirmed by checking their license number, carrier affiliation, and written disclosures.

- Ask for the agent’s full legal name and National Producer Number (NPN). Every licensed life insurance agent has one. You can verify it using the NAIC License Lookup Tool or your state’s Department of Insurance website.

- Request the carrier name. An honest agent will identify the insurance company they represent. Generic answers such as “state programs” or “benefit offices” are a scam warning sign.

- Check for written disclosures. Legitimate mailers must include the agency name, address, and license number. If any of those are missing, the sender is not compliant.

- Contact your Department of Insurance. Every state maintains a fraud investigation or consumer protection division that can confirm whether the company is registered to sell insurance in your area.

- Avoid sharing personal details over the phone until the agent’s credentials are verified.

Following these steps ensures you only work with professionals who operate legally and ethically.

WHAT TO DO IF YOU FILLED OUT A T2 FORM

Anyone who submitted a T2 Form should document contact attempts and verify every caller through state regulators.

Write down the company names, phone numbers, and any agent information. This documentation can help if you decide to file a complaint.

Next, contact your State Department of Insurance and ask to verify whether the caller or company is licensed. You can also submit a complaint through the FTC Complaint Assistant or the Consumer Financial Protection Bureau (CFPB) if you suspect deceptive activity.

If you want your information removed from marketing databases, send a written request to the company listed on the mailer.

Under U.S. consumer protection laws, you have the right to request deletion or data suppression from lead sellers. You can also add your number to the National Do Not Call Registry at donotcall.gov.

For extra protection, ask any caller who references your T2 Form how they got your information. A legitimate agent will know which lead source they are using and will answer directly.

Evasive answers almost always indicate you are dealing with a lead scam.

HOW TO REPORT A T2 FORM SCAM

Deceptive T2 mailers can be reported to federal, state, and postal authorities with copies of the form and envelope.

Collect every piece of evidence before filing your complaint. Keep the envelope, the letter, and any documentation that shows where it was mailed from. Screenshots of texts or call logs also help regulators track patterns of misconduct.

The Federal Trade Commission (FTC) accepts complaints for deceptive advertising at reportfraud.ftc.gov.

You can include scanned copies of the form and the name of any agent or company that contacted you afterward. The FTC may share your complaint with state agencies or law enforcement for joint investigations.

Each state Department of Insurance (DOI) also maintains its own complaint process. File directly through your state’s DOI website under “Consumer Services” or “Report Insurance Fraud.”

Departments in states such as Florida, Texas, and North Carolina have dedicated pages for misleading insurance advertising.

For mail-related deception, you can also report to the U.S. Postal Inspection Service, which investigates fraud involving the postal system. They maintain a separate form at uspis.gov/report for this purpose.

Providing detailed information helps authorities trace which lead vendors are using fake government-style marketing. The more reports submitted, the faster regulators can act.

I encourage anyone who receives misleading mail to report it. The faster these forms are exposed, the safer consumers become.

BETTER WAYS TO GET REAL FINAL EXPENSE QUOTES

Working with a licensed independent broker gives you clear pricing and coverage without deceptive mailers.

Independent brokers have access to several underwriting options and can match you with first-day coverage based on your health, age, and budget.

Unlike T2 Form marketers, real brokers must identify themselves by name, license, and agency before discussing rates.

They are also required by law to disclose which insurance companies they represent. This transparency ensures consumers know exactly who they are dealing with.

Below is an example comparison between T2 Form “lead” systems and working with a legitimate broker.

HOW I HELP PEOPLE AVOID T2 FORM SCAMS

I guide people through identifying fake mailers and then help them qualify for real insurance through licensed carriers.

When someone calls me after receiving a T2 Form, I start by verifying whether the contact information on that form is legitimate.

I then walk them through how the form works, who sends it, and why it exists. Once the confusion is cleared, we may then talk about real, licensed insurance options that fit their needs and budget.

Every policy I recommend is issued directly by a verified insurance carrier, never through a third-party lead vendor. I only work with companies that publish transparent rate charts, clear underwriting rules, and fair first-day coverage for qualified applicants.

I also explain what each policy actually does, what it costs, and what to expect during the application process.

Education is the foundation of my life insurance qualification process.

I teach clients how to verify agents, check licenses, and avoid call centers that push overpriced “state benefit” plans. I make sure every client understands the fine print, the waiting periods, and the cash-value structure before signing anything.

CONCLUSION: WHAT CONSUMERS SHOULD DO NEXT

Consumers should treat the T2 Form as advertising, avoid sharing personal data, and work only with verified agents.

Once the form is filled out, the information can circulate through a network of resellers, exposing you to repeated phone calls and misleading offers.

Consumers who receive a T2 Form should treat it as an advertising scam.

NEVER share personal or medical information unless you are dealing directly with a licensed agent you have verified through your state’s Department of Insurance.

Always ask for the agent’s full name, license number, and carrier affiliation before giving consent to discuss life insurance.

Working with a trusted, independent broker removes the guesswork. Licensed professionals can compare multiple carriers at once and find policies that provide immediate protection with transparent pricing and clear terms.

If you have questions about final expense coverage, or if you want to verify a mailer or agent, contact me directly at 888-862-9456 or visit FEXGUY.com. You will always speak with a licensed professional who answers your questions honestly and respects your privacy.

FREQUENTLY ASKED QUESTIONS: T2 FORM SCAM

Is the T2 Form a government document?

The T2 Form is a private marketing mailer, not an official agency document.

The T2 Form is a privately created marketing mailer that collects personal data for life insurance lead generation. It has no connection to the Social Security Administration, Veterans Affairs, or any state agency.

Who sends the T2 Form?

Private lead generation companies distribute the T2 Form to collect and sell consumer data.

Is it safe to fill out the T2 Form?

Filling out the T2 Form can trigger aggressive follow-up and repeated data resales.

Submitting the form can result in repeated calls and the reselling of your data to multiple call centers or agents.

How can I report a suspicious life insurance mailer?

You can report suspicious mailers to consumer protection and insurance enforcement agencies.

Attach a copy of the form and envelope when submitting your complaint.

What is the safest way to get a real-life insurance quote?

A licensed independent broker gives you a verifiable quote without using mass-mail data traps.